i

iAt its open meeting held on January 30, 2020, the Commodity Futures Trading Commission (“CFTC” or “the Commission”) approved a proposed rulemaking to institute federal position limits in an effort to prevent excessive speculation, squeezes, and corners in both futures positions and “economically equivalent” swaps for certain specified commodities. The vote was 3-2 with all Republicans supporting and all Democrats opposing.

The proposal approved on January 30 is the Commission’s latest effort to propose position limits as part of its implementation of the Dodd-Frank Act. The initial rules, which were to go into effect in the fall of 2012, were struck down by a federal district court just prior to their planned implementation.[1] Since then, the CFTC has issued three proposals for the institution of federal position limits, none of which have resulted in final rules.

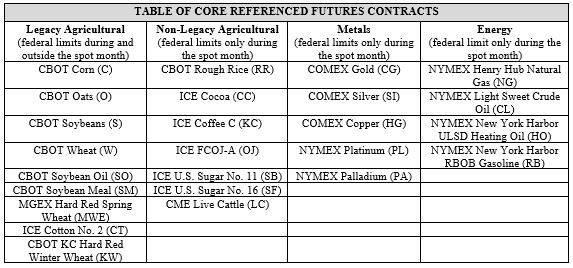

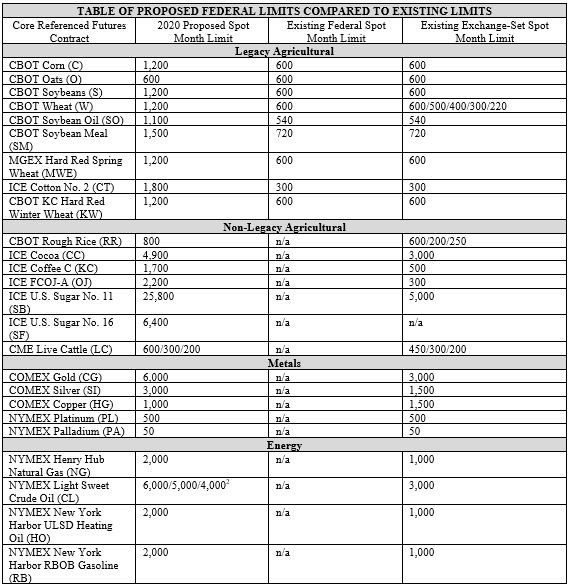

Currently, there are: (1) federal position limits on nine “legacy” agricultural futures and (2) exchange-based position limits on many commodity futures contacts. The CFTC’s latest proposal expands the scope of federal position limits to twenty-five physically-delivered commodity futures contracts, including additional agricultural commodities as well as metals and energy commodities. The proposal would cover positions in the named futures contracts themselves (“Core Referenced Futures Contracts”), other related futures contracts, and certain swaps, including bilateral agreements (“Economically Equivalent Swaps”) (collectively, “Referenced Contracts”). The federal limits are in addition to current exchange-set limits. The related futures contracts and Economically Equivalent Swaps include positions that are linked by their terms in certain specified ways to a Core Referenced Futures Contracts. The Core Referenced Futures Contracts and related limits are shown in the tables below.

Rather than being an extension of prior proposed rules, the proposal is largely a new approach to federal position limits. It has a more limited scope, is less burdensome on hedgers, and contains higher proposed limits compared to prior proposals.

Some key aspects of the federal position limits proposal are as follows:

-

A market participant cannot hold more than the specified federal position limit in a Referenced Contract during the specified spot period for such contract.

-

If the Referenced Contracts held by a person during the spot period are considered bona fide hedges, as that term is defined in the proposal, the market participant may exceed the federal position limit by such amount.

-

The CFTC has proposed 11 enumerated bona fide hedges upon which a person can rely. These enumerated bona fide hedges are self-effectuating for hedgers, meaning there are no forms to submit or CFTC approval required. The futures exchanges are expected to implement the application of the bona fide hedge exemptions with respect to both federal and existing exchange position limits.

-

The CFTC has also proposed a process whereby futures exchanges may approve bona fide hedge exemptions for positions that do not fall within the scope of the proposed enumerated bona fide hedge(s) based upon the demonstrated hedging needs of the market participant and the general criteria for bona fide hedges.

-

Any such non-enumerated bona fide hedge(s) granted by an exchange would be considered a bona fide hedge exempting covered positions from the position limits unless the CFTC rejects the approval within 10 business days (or 2 business days in the case of certain emergency hedge exemptions).

-

Futures exchanges will provide to the Commission monthly reports of non-enumerated bona fide hedge approvals.

-

The CFTC will rely upon its Enforcement Division and the futures exchanges to police the federal position limits.

-

The federal position limits will take effect 1 year from the date on which final rules based on this proposal are published in the Federal Register.

The CFTC has established a 90-day comment period on the proposal ending April 29. It has also included 55 discrete questions for which it is seeking comment.

It is too soon to tell whether this approach to federal position limits will prove to be as controversial as previous proposals. The proposal attempts to mitigate many of the concerns raised by hedgers in the past by expanding the scope of the bona fide hedge exemptions, eliminating real-time reporting on covered positions, cash positions and bona fide hedges, raising the proposed limits, and deferring to the expertise of the futures exchanges.

The split Commission vote on approving the proposal for comment may be an indication of ongoing contention surrounding the imposition of federal position limits at the Commission. Regardless, the Chairman seems committed to enacting position limits and has commenced an ambitious process to finalize this rule.

_________________________________________________________

[1] Int’l Swaps & Derivatives Ass’n v. U.S. Commodity Futures Trading Comm’n, 887 F. Supp. 2d 259 (D.D.C. 2012).

[2] 2020 Proposal at p. 14: The proposed federal spot month limit for Light Sweet Crude Oil would feature the following step-down limit: (1) 6,000 contracts as of the close of trading three business days prior to the last trading day of the contract; (2) 5,000 contracts as of the close of trading two business days prior to the last trading day of the contract; and (3) 4,000 contracts as of the close of trading one business day prior to the last trading day of the contract.