i

iAs a result of both legislative mandates as well as Congressional and public concern, the Board of Governors of the Federal Reserve System (Board) has been examining whether to impose new restrictions on the activities of banks related to physical commodities. Following these examinations, the Board recently took two actions designed to impose new limits on the activities of banks related to physical commodities: (i) a notice of proposed rulemaking to impose new capital requirements and other limits on such activities of financial holding companies (FHCs[1]) (the “proposed rule”[2]); and (ii) a report, issued pursuant to Section 620 of the Dodd-Frank Act (620 Report),[3] which contains recommendations for legislation to repeal several current authorities for banks to engage in physical commodities activities.

Proposed rule. In brief, the proposed rule would:

- increase the capital requirements for activities of FHCs involving commodities for which existing laws would impose liability if the commodities were released into the environment;

- lower the limit on the amount of physical commodities that may be held by banks that conduct commodity trading activities;

- rescind authority for banks to engage in energy tolling and energy management services;

- delete copper from the list of precious metals that BHCs are permitted to own and store; and

- establish new public reporting requirements on the nature and extent of firms’ physical commodities holdings and activities.

620 Report. The 620 Report is divided into three sections, by federal banking regulator. Section I, prepared by the Board, covers state member banks, depository institution holding companies, Edge Act and agreement corporations, and US operations of foreign banking organizations. In its section, with respect to physical commodities, the Board recommends legislative action that would:

- repeal the authority of FHCs to engage in merchant banking activities; and

- repeal the grandfather authority for certain FHCs to engage in commodities activities under section 4(o) of the Bank Holding Company Act (BHCA).[4]

Although participants in energy and other physical commodity markets have commented to the Board that the imposition of new capital requirements and other restrictions on bank participation in physical commodity markets could reduce liquidity and increase costs for end users, the Board has nonetheless proceeded with the proposed rule and legislative recommendations. The Board estimates that the proposed rule will not have a significant impact on the physical commodity markets or the related derivative markets.

Although participants in energy and other physical commodity markets have commented to the Board that the imposition of new capital requirements and other restrictions on bank participation in physical commodity markets could reduce liquidity and increase costs for end users, the Board has nonetheless proceeded with the proposed rule and legislative recommendations. The Board estimates that the proposed rule will not have a significant impact on the physical commodity markets or the related derivative markets.

In this article, we summarize and provide key takeaways from the proposed rule and the 620 Report.

The Proposed Rule

Background

Prior to 1999, BHCs were generally barred from participating in “commercial” activities and had very limited authority to engage in physical commodities activities. Pursuant to the BHCA, BHCs could undertake only those commodities activities that were “so closely related to banking as to be a proper incident thereto,” such as buying, selling and storing precious metals and copper, or acting as principals in cash-settled commodities derivative contracts.

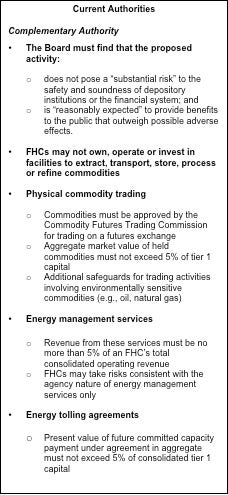

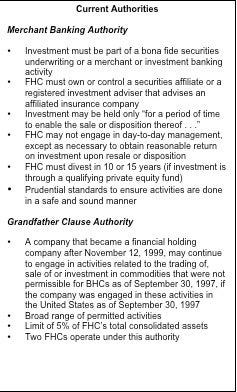

The Gramm-Leach-Bliley Act (GLBA) amended the BHCA by allowing BHCs with well-capitalized bank subsidiaries to expand the scope of their activities with respect to commodities. Specifically, three key provisions gave BHCs greater opportunities in this area: (1) the complementary authority under BHCA section 4(k), which allows FHCs to engage in any activity deemed by the Board to be “complementary to a financial activity”; (2) the merchant banking authority, which allows FHCs to invest in nonfinancial companies that engage in commodities activities that FHCs themselves are not permitted to undertake; and (3) the grandfather clause authority under BHCA section 4(o), which permits certain institutions that were conducting physical commodities activities prior to becoming FHCs to engage in a broad range of physical commodities activities, including those beyond the scope of both the complementary and the merchant banking authorities.

To date, the Board has approved three types of complementary activities: (i) physical commodities trading, which includes taking delivery of commodities under derivative contracts and buying and selling in the spot market; (ii) energy management services, such as providing advisory services to or arranging transactions for power plant owners; and (iii) energy tolling agreements, under which firms pay power plant owners fixed payments in exchange for the rights to plant output.

Advance Notice of Proposed Rulemaking. In January 2014, the Board issued an Advance Notice of Proposed Rulemaking to review the scope of physical commodities activities currently permitted by law, and determine whether such activities pose significant risks to the safety and soundness of insured depository institutions or the financial system generally, and whether additional limits or requirements should be imposed on the banks conducting these activities.[5]

Senate testimony on rulemaking. In November 2014, Federal Reserve Board Governor Tarullo testified to Congress that the Board would be issuing a notice of proposed rulemaking and was considering whether to impose more stringent overall caps on complementary and merchant banking activities, as well as stricter capital requirements by increasing the risk weighting for physical commodities activities associated with catastrophic or environmental risks.[6]

The proposal

The proposal

On September 23, 2016, the Board issued a proposed rule to (i) adopt new limits on physical commodities trading activity conducted by FHCs under the complementary authority; (ii) impose new risk-based capital requirements on FHC physical commodities activities; (iii) rescind the authorizations for FHCs to engage in energy management services and energy tolling; (iv) remove copper from the list of precious metals that BHCs are permitted to own and store as an activity closely related to banking; and (v) impose new public reporting requirements to increase transparency into physical commodities activities of FHCs.

The higher capital requirements would be imposed through new proposed risk weights for the various types of permissible commodities activities.[7] To determine the risk-weighted asset exposure for covered physical commodities, these proposed risk weights would be multiplied by (i) the market value of all section 4(o) permissible commodities; (ii) the original cost basis of section 4(o) infrastructure assets; (iii) the market value of section 4(k) permissible commodities;[8] and (iv) the carrying value of an FHC’s equity investment in companies that engage in covered physical commodities activities.[9]

The proposed rule would affect each of the GLBA authorities as follows:

Complementary authority

New risk-based capital requirements. A 300% risk weight would apply to physical commodities holdings permissible under complementary physical commodities trading activities. The proposed requirements would apply with respect to physical commodities that are substances covered under federal or relevant state environmental statutes and regulations (“covered physical commodities”). According to the Board, “These physical commodities carry the greatest potential liability under relevant environmental laws.”[10] The Board states that this would provide a level of capitalization for these activities that is “roughly comparable to that of nonbank commodities trading firms.”[11]

Tighten the cap on physical commodities holdings. In order to limit the aggregate risks from physical commodities trading activities that an FHC may face, the limit placed on physical commodities holdings of FHCs under complementary authority (5% of tier 1 capital) would also take into account physical commodities held anywhere in the FHC, subject to a few exceptions.[12] The ability of an FHC to undertake or expand its physical commodities activities under the complementary authority therefore would be constrained by the extent to which the FHC and its subsidiaries engage in physical commodities activities under other authorities.[13]

Clarify prohibition on operations. The proposal would codify in the Board’s Regulation Y the prohibition on owning, operating or investing in facilities for the extraction, transportation, storage or distribution of commodities under the complementary authority. It also would clarify that this prohibits directing the operations of third-party extraction, storage or transportation providers. The proposed list of restrictions is not intended to be exhaustive; the Board states that the purpose of this proposal is to ensure that FHCs refrain from activities related to physical commodities that could impose environmental liability upon the FHC.[14]

Rescind authority for energy management services and tolling. Energy management services and tolling would no longer be permitted under complementary authority. According to the Board, the proposal would affect the actual activity of only one firm and the authority of five FHCs. The Board states that the fact that only one firm is now engaging in these activities indicates that the activities are not “as directly or meaningfully connected to a financial activity as is physical commodities trading,” and that the expected benefits from permitting these activities have not materialized.[15] The Board mentions that the rescission of these authorities would not affect the ability of FHCs to provide derivatives and related financial products and services to power plants or engage in physical trading. The proposal provides a two-year transition period to conform to these new restrictions.

Merchant banking authority

New risk-based capital requirements. The proposal would apply a 1,250% risk weight to a merchant banking investment in a company engaged in physical commodities activities unless all of the physical commodities activities of the portfolio company are permissible under complementary authority (e.g., physical commodities trading). If all the physical commodities activities of the portfolio company are permissible under complementary authority, then: (i) a 300% risk weight would apply to the investment if the company is publicly traded (the same risk weight that would apply to physical commodities trading activities conducted under the complementary authority); and (ii) a 400% risk weight would apply if the company is not publicly traded (this is intended to be consistent with the standardized approach to equity exposures).

The capital requirements would not apply to certain end user physical commodities activities where the portfolio company uses covered physical commodities to operate businesses otherwise unrelated to physical commodities. The proposed capital requirements would not apply to a merchant banking investment solely because the portfolio company owns or operates a facility or vessel that purchases, stores, or transports a covered physical commodity only as necessary to power or support the facility or vessel.[16]

The Board explains that these risk weights are designed to address the risks from merchant banking investments generally, “the potential reputational risks associated with the investment, and the possibility that the corporate veil may be pierced and the FHC held liable for environmental damage caused by the portfolio company.”[17] In the Board’s view, a higher risk weight for privately traded portfolio companies is warranted because an FHC “may not be able to gain access to markets for a privately held portfolio company after an environmental catastrophe” involving that company.[18]

Grandfather authority

New risk-based capital requirements. A 1,250% risk weight would apply to physical commodities and related assets (e.g., infrastructure assets) permitted to be owned solely under the statutory grandfather provision. This risk weight would be applied to the market value of all commodities permitted to be held only under the grandfather authority, as well as to the original cost basis of section 4(o) infrastructure assets.

A 300% risk weight would apply to activities that are conducted under the grandfather provision or through merchant banking authority but that are also permissible under complementary authority. The 300% risk weight would apply only, however, to the extent that the market value of the amount of physical commodities held under this authority, when aggregated with the market value of other physical commodities owned by the FHC that the proposal would not already subject to a 1,250% risk weight, does not exceed 5% of the consolidated tier 1 capital of the FHC.[19]

The Board states that the 1,250% risk weight, which is the highest risk weight currently specified by the Board under its standardized approach, is “intended to address the risk of legal liability resulting from the unauthorized discharge of a covered substance in connection with the infrastructure asset.”[20] The Board notes that this risk weighting is not intended to require capital against the full potential liability that might result from a catastrophic event, but rather is intended to reflect “the higher risks of physical commodity activities permissible only under section 4(o) grandfather authority without also making the activities prohibitively costly by attempting to capture the risks of the largest environmental catastrophes.”[21]

Reclassification of copper

Copper would be deleted from the list of precious metals that BHCs are permitted to own and store for their own accounts or the accounts of others. The Board explains that although in 1997 copper was added to the list that included gold, silver, platinum and palladium bullion, coins, bars and rounds, over time copper has “become most commonly used as a base or industrial metal, and not as a store of value in the same way as gold, silver, platinum, and palladium.”[22] The Board notes, and we discuss below, that the Office of the Comptroller of the Currency (OCC) has recently proposed a similar reclassification of copper under the National Bank Act.

Public reporting

The proposed rule would impose new public reporting requirements for commodities holdings of FHCs in order to increase transparency, allow better monitoring by regulators and improve firm management of these activities.[23] The proposed rule would require the reporting of the total fair values of various commodities held in inventory, as well as the risk-weighted asset amounts associated with an FHC’s covered physical commodities activities, section 4(o) infrastructure assets or investments in covered commodity merchant banking investments.

FHCs also would be required to identify whether they own any covered physical commodities, any section 4(o) infrastructure assets or any investments in covered commodity merchant banking investments; whether they are engaged in the exploration, extraction, production or refining of physical commodities; and whether they own facilities, vessels or conveyances for the storage or transportation of covered physical commodities. Further, FHCs would be required to report the total fair value of section 4(k)- and section 4(o)-permissible commodities owned, the original cost basis of any section 4(o) infrastructure assets, and the carrying value of investments in covered commodity merchant banking investments.

Board analysis of impacts

The Board believes the proposal will not have a material impact on the markets for physical commodities or derivative instruments related to those commodities.[24] According to the Board, the amount of additional capital required to be held by FHCs under the proposal would be approximately $4.1 billion in the aggregate. The Board estimates the proposal would result in an “insignificant” increase of 0.7% in total risk-weighted assets and a 7.1% increase in risk-weighted assets attributable to trading business. The Board concludes that, among FHCs that engage in physical commodities activities, this increase in risk weighting “would not cause any FHC to breach the minimum capital requirements.”[25]

The Board observes that “if FHCs consider their physical commodities trading on a standalone basis, the proposed increases in capital requirements could make this activity significantly less attractive based on its return on capital, and could result in decreased activity.”[26] The Board states, however, that such a reduction in activity “is not likely expected to have a material impact on the broader physical commodity markets.”[27] Although the Board acknowledges that information on the markets covered by the proposal is “relatively scarce,” the Board states that it appears that Board-regulated entities account for a small fraction of the physical markets for these commodities.

Using data from the Commodity Futures Trading Commission’s (CFTC’s) Bank Participation Report, the Board finds that the market share of banks in derivative contracts involving physical commodities ranges from 2% to 15% and therefore that any reduction in bank activity in these financial markets that might result from the proposal “should not materially impact” these derivative markets.[28] The Board also estimated that, in light of the relatively small share of FHCs in the commodity markets, the impact of the proposed increase in capital requirements upon merchant banking investment activities “appears insignificant.”[29]

Section 620 Report

Overview

Enacted in the shadow of the public debate over the Volcker Rule, Section 620 of the Dodd-Frank Act was intended to address activities not covered by the Volcker Rule’s restrictions on proprietary trading and covered fund activities, in particular longer-term risky holdings and trading.[30] Section 620 requires the three federal banking regulators[31] to conduct a study and report to Congress within 18 months of the enactment of Dodd-Frank. The report must address the appropriate activities and investments for banking entities under federal and state law, as well as review and consider (i) the types of permissible activities or investments; (ii) any financial, operational, managerial or reputation risks associated with or presented as a result of the banking entity engaged in the activity or making the investment; and (iii) risk mitigation activities undertaken by the banking entity with regard to the risks. The banking regulators submitted the 620 report on September 8, 2016, over six years after enactment of the statute. The 620 Report is divided into three sections, one for each regulator, covering those entities subject to its supervision:. The Board prepared Section I, the FDIC Section II, and the OCC Section III.

The three regulators have taken markedly different approaches in the 620 Report. Consistent with its approach under the proposed rule, the Board, in Section I of the 620 Report, has made a series of recommendations for legislative repeal of several of the authorities that currently allow banking entities to engage in commercial activities, calling for a greater separation of banking and commerce. The Board’s recommendations all require congressional action.

The OCC, which supervises national banks, federal savings associations, and federal branches and agencies of foreign banks does not recommend legislative action but plans to take action itself, through rulemaking or guidance, to enhance its prudential regulatory scheme. It intends to issue unilaterally rules and guidance that could have a significant and more immediate effect on banks’ asset-backed securities, derivatives, commodities and structured products activities.[32]

The FDIC, which supervises state-chartered insured banks and savings associations, has identified several areas for potential action but has taken the least drastic approach by adopting a wait-and-see posture to consider how certain activities interact with existing and new FDIC regulations and supervisory approvals.

The Board: Section I

The Board’s recommendations in its section of the 620 Report are sweeping, calling for the repeal of authorities and exemptions that currently allow FHCs and SLHCs to engage in a broad range of commercial activities. With respect to banks’ authorities to engage in physical commodities activities, the Board recommends the repeal of the merchant banking and Section 4(o) authorities under the BHCA that had been added by the GLBA.[33]

Repeal of merchant banking authority. As discussed above, under current merchant banking authority, FHCs may make investments in nonfinancial companies as part of a bona fide merchant or investment banking activity, including in any type of nonfinancial company, including portfolio companies engaged in physical commodities activities. In addition, ownership investments in a portfolio company may be in any amount. Current regulations require that corporate separateness be maintained to help ensure the limited liability of the FHC’s investment. Thus, an FHC generally may not participate in the day-to-day management of a portfolio company. FHCs are also required to establish risk management policies and procedures for these merchant banking activities. Under the GLBA, however, an FHC may manage or operate a portfolio company as may be necessary to obtain a reasonable return on the resale or disposition of the investment. According to the Board, this exposes the FHC to increased risks of being liable for operations of the portfolio company (e.g., if the portfolio company were involved in an environmental event). In the Board’s view, its regulatory authority to limit the potential risks to the FHC is not sufficient to manage the safety and soundness concerns, leading the Board to call for the wholesale legislative repeal of merchant banking authority.

Repeal of Section 4(o) grandfathering. The 620 Report also calls for a repeal of the grandfather authority under BHCA Section 4(o). The Board is concerned that this authority raises safety and soundness concerns largely because certain environmental laws impose strict liability on the owners and operators of certain physical commodities facilities for environmental releases or other events. Liability arising from environmental catastrophes can, in the Board’s view, create material financial, legal, reputational and market access harm for these firms. The Board is also concerned that lack of separation between banking and commerce creates a risk of undue concentration that could have a disproportionate effect on financial markets, production and employment if failure occurs. In addition, the Board argues that, because the Section 4(o) authority applies to only two firms, it raises competiveness concerns, including access to important industry-related information to which other FHCs do not have access, such as the amount and timing of production. The Board is also critical of the automatic nature of the Section 4(o) grandfather, which allows a covered company to engage in physical commodities activities without notice to or approval of the Board.

The OCC: Section III[34]

The OCC does not recommend any congressional action in its section of the 620 Report. Instead, it notes its intention to take regulatory action in each of the four areas it reviewed, namely physical commodities, derivatives, securities and structured products. We discuss its approach to physical commodities and derivatives below.

Physical commodities. Like FHCs, national banks currently may buy and sell coin and bullion, which, under OCC precedent, include gold, silver, platinum, palladium and copper. Banks may store these precious metals for themselves and their customers and may transport the metals to or from their customers. Banks may also serve as custodian for an exchange-traded fund that invests in these precious metals. Consistent with the proposed rule issued by the Board, the OCC plans to solicit comment on whether it should treat copper as a base metal rather than as “coin and bullion.” The OCC’s proposal will define “coin and bullion” to exclude copper cathodes and will conclude that buying and selling copper is generally not part of or incidental to the business of banking.

National banks may also buy and sell physical commodities (within limits) to hedge commodity price risk in connection with customer-driven commodity derivative transactions. The 620 Report notes that the OCC published supervisory guidance in 2015 to clarify how national banks should calculate how much of their hedging involves physical settlement so that they remain within the current precedent that requires that physical hedges be no more than 5% of a bank’s hedging activity.[35] The 620 Report notes that this guidance implements the OCC’s recommendation that physical hedging limits be clarified.

National banks may also acquire exposure, up to a limit of capital and surplus, to physical commodities through investment in renewable fuel capital investment companies, up to 5% of capital and surplus and certain investments that promote primarily the public welfare, such as in companies that generate renewable energy. In addition, national banks may acquire physical commodities in satisfaction of a debt previously contracted (e.g., the bank could foreclose on grain collateral pledged for a loan to a farmer). The 620 Report does not contain recommendations relating to these activities.

Derivatives. National banks may enter into derivatives transactions with payments based on bank-permissible holdings (e.g., tied to interest rates, foreign exchange, credit, precious metals and investment securities). With OCC-written non-objection, banks may deal in derivatives on certain other assets if part of customer-driven financial intermediation. National banks may not conduct proprietary trading in these derivatives. The OCC notes that Congress has approved national banks’ ability to offer swaps in connection with originating a loan. However, the OCC is concerned with what it views as smaller national banks’ interest in expanding their swap dealing business, particularly in commodity swaps. In 2014, the OCC enhanced its procedures for examining activities in which the bank enters into derivatives as an end user rather than as a dealer. The OCC now intends to “clarify minimum prudential standards” that apply to national banks engaging in certain swap dealing activities.[36]

The OCC is also reviewing the risks to federal banking entities of the entities’ membership in clearinghouses, particularly where their liability is not capped by the rules of the clearinghouse. The OCC may decide to issue guidance on clearinghouse membership.

Conclusion

Despite substantial input from market participants to the effect that physical commodities activities of banks have been conducted in a safe and sound manner and do not pose a significant potential for catastrophic liability or systemic risk, the proposed rule and the Board’s legislative recommendations in the 620 Report indicate the Board’s ongoing commitment to make significant changes in this area and suggest that the Board is unlikely to be receptive to overall philosophical opposition to its proposed direction. While the Board has previously floated broad ideas on reform, the proposed rule represents the first time the Board has offered specifics on how it intends new limitations to work and an estimate of the market impacts of such proposals. The Board therefore may be more receptive to comments concerning the effects of the specific measures it has proposed, including its estimates of the market impacts from these specific proposals. Comments on the proposed rule must be submitted by December 22, 2016.

The Board’s preferred direction with respect to changes to the BHCA is also clear. However, the impending election makes it impossible to predict the likelihood of legislative movement in this regard.

[1] An FHC is a bank holding company (BHC) with well-capitalized subsidiaries that, pursuant to the Gramm-Leach Bliley Act (GLBA), may engage in financial activities, including securities underwriting and dealing, insurance activities, and merchant banking activities.

[2] Notice of proposed rulemaking, Risk-based Capital and Other Regulatory Requirements for Activities of Financial Holding Companies Related to Physical Commodities and Risk-based Capital Requirements for Merchant Banking Investments (Sept. 23, 2016) (hereinafter referred to as “NPRM”); available at https://www.federalreserve.gov/newsevents/press/bcreg/bcreg20160923a2.pdf.

[3] Report to the Congress and the Financial Stability Oversight Council Pursuant to Section 620 of the Dodd-Frank Act (September 2016), available at https://www.federalreserve.gov/newsevents/press/bcreg/bcreg20160908a1.pdf.

[4] The Board also makes legislative recommendations with respect to other types of activities. It recommends the repeal of (i) the exemption that permits corporate owners of industrial loan companies (ILCs) to operate outside of the regulatory and supervisory framework applicable to other corporate owners of insured depository institutions; and (ii) the exemption for grandfathered unitary savings and loan holding companies (SLHCs) from the activities restrictions applicable to all other SLHCs.

[5] Complementary Activities, Merchant Banking Activities, and Other Activities of Financial Holding Companies Related to Physical Commodities, 79 Fed. Reg. 3330 (Jan. 21, 2014). In response to the notice, critics of bank involvement in commodities argued that financial holding companies participating in these markets had an unfair competitive advantage, presented serious conflicts of interest and, most important, exposed the financial system to serious risk in the event of a catastrophic event. They believed that further regulation would help mitigate these risks, thereby protecting the financial system. Citing benefits such as increased convenience and competition, efficiency gains, more readily available liquidity, and lower commodity prices, proponents of bank involvement in physical commodities claimed that financial holding companies provide valuable services to end users, such as municipalities, that would be difficult to replace in the event of stricter regulation that might preclude banks from participating in physical commodities activities. Proponents pointed to the robust risk management processes that banks have established to ensure the safety of physical commodities activities, and further cited the sound safety record to date as evidence that these activities do not pose undue risks to financial holding companies or the financial system.

[6] Wall Street Bank Involvement with Physical Commodities: Hearing before the Perm. Subcomm. on Investigations of the S. Comm. on Homeland Sec. and Governmental Affairs, 113th Cong., 2d Sess. (Nov. 2014) (testimony of Gov. Tarullo).

[7] In general, the amount of capital an institution subject to capital requirements is required to hold is calculated by multiplying the minimum capital adequacy ratio (e.g., 4% or 8%) by the risk-weighted asset exposures. Thus, for example, if the minimum capital adequacy ratio is 8%, a risk weight of 1,250% applied to the market value of section 4(o)-permissible commodities would mean that for these activities the FHC would be required to hold an amount of capital equal to the total market value of the commodities held under that authority.

[8] The proposal provides for an FHC to use daily averages for physical commodities quantities and rolling month-end, end-of-day spot prices over a 60-month period to determine the market value of its covered physical commodities. NPRM, at p. 32.

[9] Id., at pp. 31–32.

[10] Id., at p. 25.

[11] Id., at p. 27.

[12] The proposal would exclude from the cap the physical commodities activities of portfolio companies held under the merchant banking authority, assets related to the satisfaction of debts previously contracted and insurance company investments held under BHCA § 4(k)(4)(I).

[13] Examples of such other authorities cited by the Board are the authority for certain national banks to hold physical commodities to hedge customer-driven, bank-permissible derivative transactions, and the authority to possess physical commodities provided as collateral in satisfaction of debts previously contracted in good faith. NPRM, at p. 20.

[14] Id., at p. 23.

[15] Id., at p. 42.

[16] Id., at p. 30.

[17] Id.

[18] Id.

[19] The proposal calls this the “section 4(k) cap parity amount,” which excludes commodities owned pursuant to the merchant banking authority, similar insurance investment authority, and authority to acquire assets and voting securities in satisfaction of debts previously contracted.

[20] NPRM, at p. 27.

[21] Id.

[22] Id., at p. 46.

[23] Memorandum from Staff to Board of Governors, Re: Proposed Rule Implementing Strengthened Prudential Requirements, including Risk-based Capital Requirements for Physical Commodity Activities and Investments of Financial Holding Companies, at p. 2.

[24] NPRM, at pp. 34–35.

[25] Id., at p. 34.

[26] Id.

[27] Id.

[28] Id., at p. 35.

[29] Id.

[30] See 156 Cong. Rec. S5895 (July 15, 2010) (statement of Sen. Merkley).

[31] The three federal banking regulators are the Board, the Federal Deposit Insurance Corporation (FDIC) and the OCC.

[32] Specifically, the OCC plans to:

- issue a proposed rule that restricts national banks from holding as type III securities asset-backed securities, which may be backed by bank-impermissible assets, and to issue an analogous proposed rule for federal savings associations;

- address concentrations of mark-to-model assets and liabilities with a rulemaking or guidance;

- clarify minimum prudential standards for certain national bank swap dealing activities;

- consider providing guidance on clearinghouse memberships;

- clarify regulatory limits on physical hedging;

- address national banks’ authority to hold and trade copper; and

- incorporate the Volcker Rule into the OCC’s investment securities rules.

[33] The Board also recommends the repeal of the exemption that allows corporate owners of ILCs to operate outside of the regulatory and supervisory framework applicable to non-ILC corporate owners and the exemption for grandfathered unitary SLHCs from activities restrictions applicable to other SLHCs.

[34] Since the FDIC did not make any recommendations, we do not discuss Section II of the Report.

[35] OCC Bulletin 2015-35, “Quantitative Limits on Physical Commodity Transactions” (Aug. 4, 2015).

[36] 620 Report at 86.