i

iIn January of 2021, Senate Bill 2291 was introduced into the North Dakota state senate. It was considered, adopted, and signed into law three months later in March of 2021. This bill was the first of what would become scores of environmental, social, and corporate governance (ESG)-related bills considered and, in some cases, signed into law in states across the United States. The 2023 state legislative session was particularly busy with respect to these bills, but now that most of the state legislatures are adjourned or in recess, the legislative activity should slow to a point where investment managers can take stock of the new laws and the pending legislation and assess what, if anything, they should do in response.

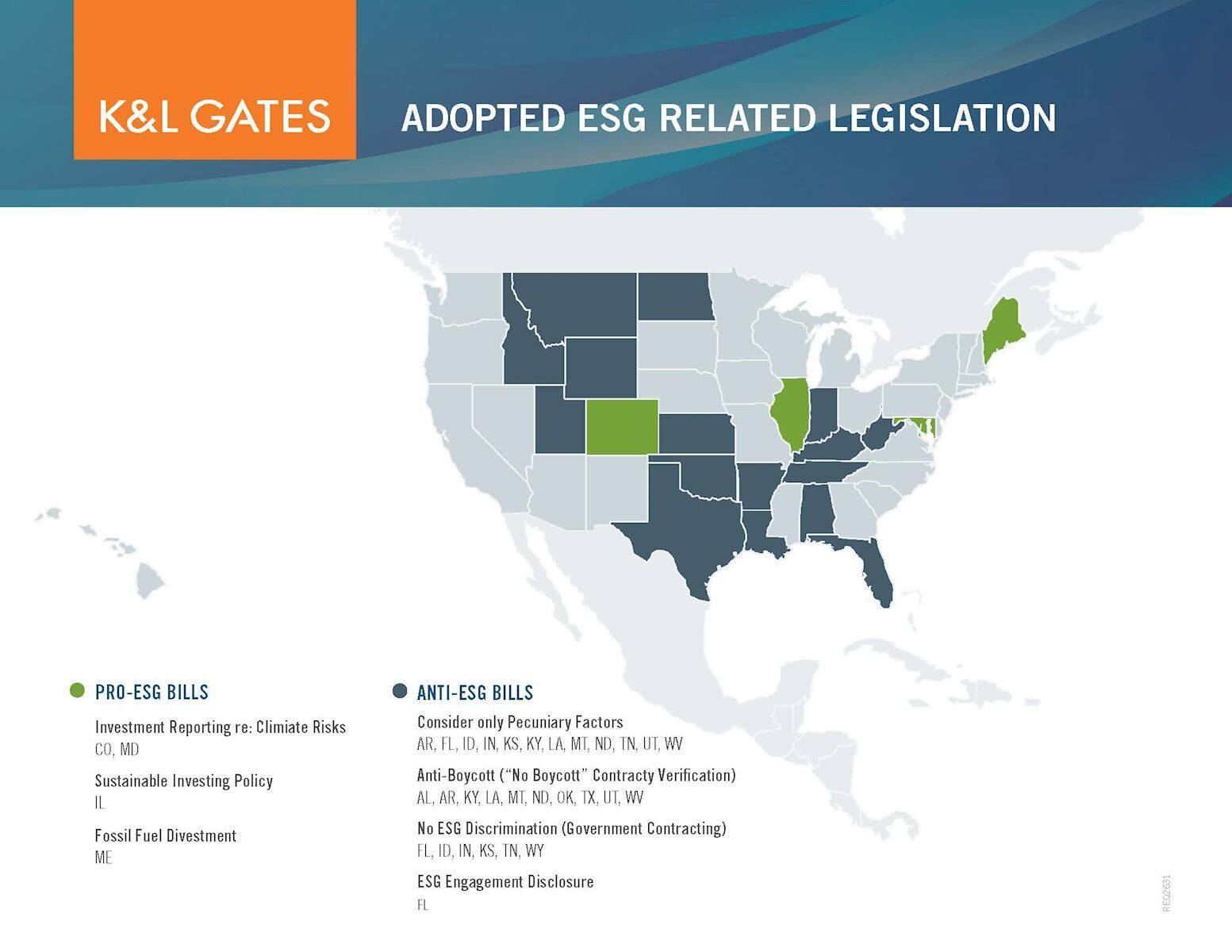

CURRENT STATE OF THE STATES—WHAT HAS BEEN ADOPTED?

The state legislative activity regarding ESG is broad in scope and applies to several different types of participants in the financial system, such as banks, insurance companies, and asset managers. We focus here on the laws that impact asset managers and their ability to do business in different states.

ESG-related legislation broadly mirrors the politicization of ESG investing. States with legislatures that lean Republican tend to be considering and adopting “anti-ESG” legislation, while states with Democratic-leaning legislatures are considering and adopting “pro-ESG” legislation. A map of the United States indicating which states have adopted which types of legislation is included below.

By the Numbers: Adopted ESG-Related Legislation:

-

22: States that have adopted some form of ESG-related laws;

-

18: States that have adopted “anti-ESG” legislation;

-

14: States that adopted “anti-ESG” legislation in the 2023 legislative session

-

4: States that have adopted “pro-ESG” legislation

-

1: State that adopted “pro-ESG” law in 2023

ANTI-ESG LEGISLATION

With respect to laws and bills that impact asset managers, the “anti-ESG” bills adopted to date take several forms and differ with respect to key details from state to state; however, they tend to share core common features. First, despite the implications from the political rhetoric surrounding these bills, the term “anti-ESG” is somewhat overbroad when applied to these state legislative efforts. In fact, none of the “anti-ESG” laws adopted so far entirely ban the use of ESG factors in making investments. Instead, these laws generally place conditions and limitations on how ESG factors may be considered in the investment process, generally limiting the consideration ESG factors to financial or “pecuniary” decision making. In other words, even in the 18 states that have adopted “anti-ESG” legislation, there remains room for investment managers to make decisions on investments based on ESG factors so long as that consideration is grounded in the pursuit of financial returns.

In addition, all of the bills adopted to date apply only to the disposition or management of state funds, e.g., who the state can hire, in which companies can the state invest, or what standards must be applied by fiduciaries who are investing state money, particularly the assets of state pension plans. Further, to the extent these bills seek to regulate the conduct of asset managers, they tend to do so indirectly, by requiring the state agencies with whom the asset managers contract to include specific provisions in their asset management or other services agreements.

Apart from these common features, the adopted state “anti-ESG” legislation can be further categorized into five functional categories.

Pecuniary Factor Legislation

Pecuniary Factor Legislation is the most popular state approach to “anti-ESG” legislation, with variations of this approach adopted in 12 different states and under consideration in 11 more (see below map for details). While the details and implementation vary from state to state, in the main, the Pecuniary Factor Legislation requires fiduciaries to state pension plans or to other state agencies to make investments based “solely on pecuniary factors”. This language is borrowed from (now rescinded) rule amendments adopted by the United States Department of Labor (DOL) in 2020 applicable to fiduciaries to retirement plans governed by the Employee Retirement Income Security Act of 1974, as amended (ERISA).1 That rule required ERISA plan fiduciaries to select investments based solely on consideration of “pecuniary factors,” and the state laws tend to follow the same formulation. Critically, neither the DOL rule nor the state legislation based on it fully prohibits the consideration of ESG factors, unless such consideration is intended to accomplish a social purpose rather than achieve a financial result. The DOL acknowledged in the rule’s adopting release that there are “instances where one or more environmental, social, or governance factors will present an economic business risk or opportunity that corporate officers, directors, and qualified investment professionals would appropriately treat as material economic considerations.”2

As a corollary, most of the states adopting Pecuniary Factor Legislation have similar provisions applicable to the exercise of proxy voting by the state pension plans, requiring all proxy efforts to also be grounded solely in “pecuniary” or financial motivations.

Anti-Boycott Legislation

Anti-Boycott Legislation is only slightly less popular than the Pecuniary Factor Legislation, being adopted in various forms in 11 states and under consideration in seven others. Anti-Boycott Legislation finds its roots in a Texas statute from 2017 that prohibited the State of Texas from entering into contracts with or investing in companies it determined were engaged in a boycott of Israel.3 In 2021, the State of Texas passed Senate Bill 13, which similarly prohibited the State of Texas from entering into contracts with or investing in companies who, as determined by the Texas comptroller of public accounts, were engaged in a boycott of fossil fuel energy companies.

As with the Texas statutes, Anti-Boycott Legislation targets companies that “boycott” a given industry or group of industries. The prohibited “boycott” varies from state to state and can include a variety of different industries, such as fossil fuel energy companies, firearms companies, companies engaged in production agriculture, or any industry a state wants to protect.

The specific prohibitions relating to companies who engage in the prohibited “boycotts” vary from state to state. Most commonly, the Anti-Boycott Legislation will require that any state governmental entity entering into a contract with a vendor for an amount in excess of US$100,000 include a verification or representation from the vendor that the vendor does not engage in the prohibited “boycott.” In some states, including Texas, a state governmental entity will also be charged with creating a list of companies that engage in the prohibited “boycott.” These states have been sending “verification requests” to various financial services companies seeking specific information in connection with their determination as to whether the financial services firm is engaging in the prohibited “boycott.” Finally, four states (Arkansas, Kentucky, Oklahoma, and Texas) require their state pension plans to divest of the securities issued from any entity that appears on the assembled list of companies that engage in the prohibited boycott.

ESG Discrimination Legislation

ESG Discrimination Legislation has been adopted in two different forms across six different states and similar bills are under consideration in five other states. In general, ESG Discrimination Legislation prohibits discriminating against certain parties on the basis of ESG factors, ESG scores, or other criteria unrelated to the specific business at hand. Some varieties of these bills apply to governmental entities in the selection of vendors and others apply to financial entities in connection with their acceptance of clients or customers. Under a typical ESG Discrimination Legislation applicable to a financial entity, a bank, by way of example, could not determine to deny banking services to a firearms-related company merely because the company was in the firearms business.

ESG Engagement Disclosures—Florida

While each state’s “anti-ESG” legislation generally falls within the above categories, the Florida “anti-ESG” law has a unique feature that could be adopted in future state-level “anti-ESG” legislation.4 Under the new Florida law, Florida pension plans are required to include a provision in their investment management agreements that the asset manager must make specific disclosure in the asset manager’s engagement communications. The disclosure, required in any of the asset manager’s communications with issuers regarding ESG matters, disclaims the asset manager’s representation of the Florida pension plans. This provision has not been adopted outside of Florida, but given the recent focus by various state governments on ESG-related proxy voting and engagement, it may appear in future bills.

Pro-ESG Legislation

The “pro-ESG” bills also come in several forms, but to date, only four states have adopted any such bills. These bills do not directly regulate asset managers, but instead generally direct pension plans to divest from certain industries (e.g., fossil fuels or firearms), provide reporting regarding the climate risks associated with their investment portfolios, or adopt sustainable investment policies. While this “pro-ESG” universe is currently limited, as discussed in more detail below, legislative attention to “pro-ESG” bills is accelerating and will likely be under debate in several states in the coming legislative sessions.

The Regulatory Approach—Missouri

While not directly related to state legislative activity, one state has taken an alternative approach to “anti-ESG” legislation. The state of Missouri had several “anti-ESG” bills under consideration, most of which were variations on the Pecuniary Factor Legislation or the ESG Discrimination Legislation. None of these bills passed at the close of the legislative session, but the Missouri secretary of state adopted a regulation substantially similar to one of the failed bills.5 This appears to be the first instance of a state regulatory body moving independently of the state legislature on “anti-ESG” matters. Further complicating matters, and as discussed in more detail below, the state of Missouri’s new rule is the first that seeks to substantively regulate the conduct of asset managers (rather than, as in the existing bills, regulating only state disposition of funds and/or indirectly requiring/prohibiting asset manager conduct through state contracting requirements).

LOOKING FORWARD—ESG-RELATED LEGISLATIVE TRENDS

The 2023 state legislative session is all but closed out, with only nine state legislatures still in session. Given the political nature of ESG-related legislation and that 2024 is a presidential election year, asset managers should expect a similar or greater level of state legislative activity in the next legislative session. Based on the 19 bills that were considered but not passed in state legislatures, there are certain trends that may appear in the upcoming legislative session.

Substantive Regulation—Disclosure and Consent Requirements

Two states (Missouri and Kansas) considered bills that would substantively regulate asset managers.6 Specifically, these bills would have required asset managers to make certain disclosures to their clients, and in the case of the Missouri bill, obtain consent from clients where the asset manager considers ESG factors. These bills are significant because, as noted above, the bills passed to-date have only regulated the disposition of state funds or the provisions required in contracts with state entities. Neither of these bills passed in the 2023 legislative sessions; however, as noted above, the Missouri secretary of state issued a regulation that was substantially similar to the failed legislation.

The direct regulation of asset managers poses new challenges to asset managers, especially federally registered asset managers. First, direct state regulation of asset managers could lead to significant fragmentation of asset manager compliance obligations across the United States. Second, the direct regulation of asset managers poses important legal questions concerning the pre-emption of asset manager regulation at the state level for federally-registered asset managers. The US Securities and Exchange Commission (SEC) has long taken the view that the National Securities Markets Improvement Act of 1996 provided the SEC with exclusive jurisdiction over federally-registered investment advisers, leaving states free to regulate their locally registered advisers.7 A court challenge to one or more of these state laws would represent the first significant challenge to this preemption.

By the Numbers: Pending ESG-Related Legislation:

-

22: States have ESG-related legislation under active consideration:

-

14 ”anti-ESG”

-

10 “pro-ESG”;

-

-

19: States where ESG-related legislation was proposed but did not pass

-

9: State legislatures that remain in active session

-

17: State legislatures in recess; and

-

27: State legislatures have adjourned.

DEVELOPMENTS IN PRO-ESG LEGISLATION

While the 2023 legislative session was dominated by “anti-ESG” legislation, 11 states considered “pro-ESG” legislation, and the upcoming legislative sessions may see an uptick, especially in states with Democratic-leaning state legislatures. The vast majority of the “pro-ESG” bills to date have been directives to state pension plans or other state investment bodies to divest of holdings in certain industries (e.g., fossil fuels or firearms) or with relatively high carbon emission profiles. Other bills would mandate that state self-directed investment programs offer a minimum number of investment options that incorporate ESG considerations.

EXPANSION OF ANTI-BOYCOTT SCOPE

As discussed above, the Anti-Boycott Legislation seeks to limit the state’s ability to invest in or do business with entities that “boycott” a given industry. Initially, Anti-Boycott Legislation focused on a narrow scope of industries (e.g., fossil fuel energy or production agriculture). Some states have considered bills that would be applied to companies who engage in a more generally defined “economic boycott.” As defined in the bills, an “economic boycott” would be a company’s refusal to do business with a company because it is part of an industry (e.g., fossil fuels) or because it does not meet certain social metrics, such as minimum board diversity or providing access to abortions.

REGULATORY APPROACH

While only one state (Missouri) has taken “anti-ESG” regulatory action to this point, more state regulators may open a new front by adopting their own regulations to achieve the same goals, especially in states where the ESG-related legislation fails to pass. Certain states have shown that their executive branches will act on ESG-related matters, with several states adopting specific investment policy statements with anti-ESG characteristics or state attorneys general issuing opinions that existing law prohibits investing state funds for the purposes of promoting ESG goals. Given the politics surrounding ESG, it is possible that state securities regulators may seek to fill a perceived void where state legislatures have not acted.

WHAT TO DO?

Asset managers who manage assets for states (e.g., pension plans) should carefully review these laws and regulations. While each state ESG-related law is unique and deserves its own specific analysis, in general, no state has yet adopted a law that categorically prohibits the consideration of ESG factors in connection with making investment decisions. As a result, asset managers whose ESG efforts are limited to “ESG integration” products (i.e., where ESG factors are considered solely for the purposes of generating financial returns) should not be impacted by the current wave of “anti-ESG” laws. That said, asset managers who integrate ESG factors into their investment processes should consider enhancing certain processes to ensure they can substantiate their use of ESG factors “solely for” financial purposes. First, asset managers may consider creating and maintaining documentation of their investment philosophy and process, especially with regard to how ESG factors are considered. Second, asset managers should consider adopting a heightened review of the presentation and discussion of ESG factors in marketing and disclosure documents to ensure the discussion is complete and accurate. On the other hand, asset managers who offer ESG-motivated products (e.g., impact funds) should acknowledge that state governmental entities, in states with “anti-ESG” laws, will most likely be unable to invest in these products, but even here, clear and accurate disclosure is critical to ensure that these entities do not make investments in these products that could be prohibited under state law.

In other words, the pathway through the complex and changing nature of state ESG-related legislation is the same as required under applicable federal law: (i) clear and accurate disclosure of how ESG is incorporated into an investment strategy; and (ii) implementation of the processes described in the disclosure.

ADOPTED ESG-RELATED LEGISLATION (AS OF 14 JULY 2023)

1 Financial Factors in Selecting Plan Investments, 85 Fed. Reg. 72846 (Nov. 13, 2020).

2 Id. at 72848. These amendments were rescinded and replaced by the DOL in 2022. See, Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights, 87 FR 73822 (Dec. 1, 2022).

3 H.B. 89, 85th Legis. Sess. (Tex. 2017), adopted in May of 2017 as Tex. Gov’t Code § 2270.001 et. seq.

4 See H.B. 3, 2023 Leg. (Fla. 2023).

5 See 48 Mo. Reg. 962-63, 48 Mo. Reg. 963-64. These Orders of Rulemaking are substantially based off a bill that was considered but not passed on the Missouri General Assembly, H.B. 863, 102nd Gen. Assemb. (Mo. 2023).

6 See H.B. 863, 102nd Gen. Assemb. (Mo. 2023); S.B. 291, 2023 Reg. Sess. (Kan. 2023).

7 See Rules Implementing Amendments to the Investment Advisers Act of 1940, SEC Rel. No. IA-1633 (May 15, 1997).