i

iOn June 23, 2016, New York State enacted legislation imposing a duty on banks and mortgage companies to maintain one- to four-family residential properties abandoned by their owners before they have foreclosed on the properties. By imposing a duty on lenders to maintain such “zombie properties,” the state has exposed banks and mortgage lenders to potential liability for tort claims that were likely never contemplated. In light of this new legislation, banks, mortgage lenders and insurance companies will have to reevaluate their liability exposure and insurance needs.

The new law, section 1308 of the Real Property Actions and Proceedings Law (RPAPL § 1308), will impose a $500 per day penalty on noncompliant banks once they are aware of a vacancy. Governor Cuomo signed the law in an effort to help protect neighborhoods from the harm of foreclosure. “For each zombie home that we cure,” the Governor stated, “and for each that we prevent with this legislation, we are saving entire neighborhoods from the corrosive effect of blight and neglect.”

To whom does this law apply?

The law applies to state and federally chartered banks, savings banks, savings and loan associations, and credit unions. It only applies to the first lien mortgage holder that is authorized to accept payment of the loan (the servicer). It does not apply, however, to banks that have less than .3 percent of the total loans they originated, owned, serviced or maintained in 2014.

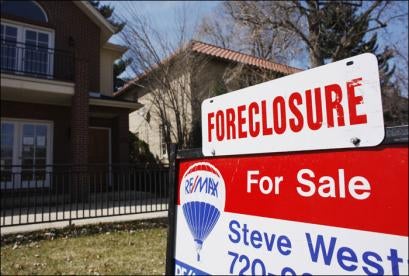

What are zombie properties?

The new law requires banks to maintain “vacant and abandoned one- to four-family residential real property.” What does “vacant and abandoned” mean? The law has amended RPAPL § 1307 to supply the following definition: a property is vacant and abandoned when (1) at least three monthly payments are past due on the mortgage or the mortgagor has advised in writing that he or she does not intend to occupy the property, and (2) there is a reasonable basis to believe that the property is unoccupied (the law provides these visual cues to determine if a property is unoccupied: overgrown or dead vegetation; accumulation of newspapers, circulars, flyers, mail or garbage; boarded, missing or broken windows; past-due utility notices or disconnected utilities) or the property is a health risk on account of evidence of vandalism, loitering, criminal conduct or destruction/ deterioration of the property. The second element also can be satisfied by a governmental agency’s declaration that the property is unfit for occupancy.

What must the bank do?

The law essentially creates two new obligations for lenders: first to monitor and second to maintain.

Monitor: When a borrower is delinquent, the servicer must inspect the exterior of the home to determine whether the property is vacant within 90 days of the delinquency and every 30 days thereafter for the duration of the delinquency. The servicer has to conduct this exterior inspection “at different times of the day.”

Maintain: If the servicer has a “reasonable basis to believe” that the home is vacant and abandoned, they must post a notice on the property with a telephone number where they can be reached. If they do not receive a call from the borrower within seven days, indicating the home is not vacant, then the loan servicer must maintain the property.

Maintenance encompasses a laundry list of actions, including replacing door locks, securing windows and doors, providing basic utilities and preventing mold growth. The full list is codified at RPAPL § 1308(4). The bank must continue to maintain the property until ownership is transferred.

What if the bank fails to comply?

If a bank violates the above-listed obligations, the superintendent of financial services may, after giving seven days notice, pursue an action in civil court. If a violation is proven, the court may issue a penalty of up to $500 for each day that the violation persists, and the municipality in which the home is located may sue for costs it incurred in maintaining the vacant home.

More significantly, however, the law also exposes banks to private liability for accidents that happen before foreclosure.

Traditionally, only a mortgagee that possessed the property was responsible for maintaining it. Trustco Bank, N.A. v. Eakin, 256 A.D.2d 778 (3d Dept. 1998); Moran v. Regency Sav. Bank, F.S.B., 20 A.D.3d 305 (1st Dept. 2005). This traditional rule changed in 2010, when New York enacted RPAPL § 1307’s “Duty to maintain foreclosed property.” With the enactment of section 1307, a mortgagee became responsible for maintaining a property after foreclosure but before it takes possession. Town of Huntington v. Lagone, 29 Misc. 3d 779 (Dist. Ct., Suffolk Cty. 2010) (holding that “the statute expressly limits a mortgagee’s duty to maintain the property only ‘after’ a foreclosure sale occurs”).

Now, however, mortgagees are responsible for monitoring and maintaining zombie properties. Therefore, a bank may be exposed to a variety of claims as it discovers that the home is abandoned. These claims include unanticipated and uninsured claims for personal injury, negligent security, property damage and nuisance. To avoid these claims, banks that lend money to New York residents must become proactive. They should monitor delinquencies to determine whether the mortgagor will soon abandon the property in order to prepare for a foreclosure sale at an earlier point in time. Banks, mortgage companies and their insurers should likewise reevaluate their potential liability exposure.