/>i

/>iAs public companies across the economic spectrum strive to overcome the supply chain disruptions drastically affecting revenue and profitability, they must not lose sight of how these disruptions impact their disclosure obligations under federal securities laws. The Securities and Exchange Commission (SEC) has demonstrated particular interest in this topic by issuing broad guidelines in recent years designed to encourage transparency with respect to how current events are impacting a company’s supply chain, and what that might mean for the business. Given the SEC’s focus on supply chain related disclosures, it is important to ensure your company is doing more than simply warning about the potential for supply chain disruptions, if such disruptions in fact presently exist.

This article discusses the SEC disclosure guidance on (1) the COVID-19 pandemic and related disruptions, (2) the Russia-Ukraine conflict, and (3) climate-related risks, and provides key takeaways for companies seeking to ensure their disclosures are accurate and compliant. This guidance is only the beginning, however, as the supply chain challenges resulting from any of these events may continue and evolve, requiring that companies redouble their efforts to provide accurate public disclosures to avoid potentially disruptive and costly SEC scrutiny.

The COVID-19 Pandemic and Related Supply Chain Shortages

Companies around the world are still feeling the impacts of the COVID-19 pandemic. When the pandemic began in March 2020, the SEC’s Division of Corporation Finance (CorpFin) released guidance regarding risk factors on which companies should particularly focus, and what additional disclosures may be required in light of COVID-19.1 In this guidance, CorpFin outlines a series of questions companies should consider when determining when it is appropriate or necessary to disclose a COVID-19 related risk. One of the questions relates directly to supply chain challenges:

Do you anticipate a material adverse impact of COVID-19 on your supply chain or the methods used to distribute your products or services?2

Since this guidance was first published, nearly every public company has identified risk factors concerning COVID-19 and related uncertainty with respect to potential impact on operations. Although COVID-19 shutdowns and spending shifts generated much of the supply chain disruption companies identified, shortages of many component parts have taken on a life of their own. Nowhere is this more apparent than with semiconductors. Many companies have been hit hard by the semiconductor shortage and blamed their unexpectedly weak quarterly results in late 2021 and 2022 on these shortages. Even as the U.S. manufacturing community has largely moved on from COVID-19, many of the key suppliers to U.S. manufacturers are located in countries, including China, that continue to be dramatically impacted by COVID-19. For more information regarding how China’s COVID-19 policy is affecting manufacturers, see our fourth article in the Supply Chain Disruption series “Managing Supply Chain Disruption in an Era of Geopolitical Risk”.

In light of these events, companies must continue to ask: (1) is COVID-19 impacting our business, including our supply chains relating to semiconductors or other components?; and (2) do changing circumstances in countries such as China require changes to disclosures which were made early in the pandemic? Companies should be asking these questions because the CorpFin, specifically its Office of Manufacturing, is already asking them.

A review of numerous CorpFin comment letters demonstrates that CorpFin’s focus is on disclosures regarding COVID and semiconductor supply chain issues. One theme is clear, it is not enough to merely identify “risk factors” under Item 105 of Regulation S-K (the SEC’s rule that requires, if appropriate, that public companies state why investment in their securities might be speculative or risky).3 SEC reviewers are asking directly whether public companies are being impacted by supply chain issues and citing semiconductor shortages as an example of such issues. The SEC reviewers also want to know if supply chain risks previously characterized as “potential” or “hypothetical” have in fact become “actual” impacts on the operations of public companies.

The same is true with respect to obligations of public companies in Management’s Discussion & Analysis (MD&A) under Item 303(b)(2)(ii) of Regulation S-K. This item requires a public company to disclose on a quarterly basis any “known trends or uncertainties that have had or that are reasonably likely to have a material favorable or unfavorable impact on net sales or revenues or income from continuing operations."4 Item 303 has long been a point of emphasis for the SEC in its efforts to encourage public companies to provide “a narrative explanation of a company's financial statements that enables investors to see the company through the eyes of management."5 Although SEC enforcement actions are rarely brought solely under Item 303, such claims are nonetheless important in assessing enforcement risk because they do not require a showing of materiality or intentional wrongdoing. In today’s economic environment, SEC reviewers are asking whether supply chain disruptions have materially affected business goals, results of operations, and capital resources. Further, CorpFin is at times asking companies to quantify such impacts to the extent possible.

Many manufacturers, particular those relying on semiconductors, including but not limited to automobile manufacturers, have seen financial results suffer in recent quarters due to an inability to obtain semiconductors and other key components to fill orders. Unsurprisingly, numerous securities class action lawsuits have been filed, claiming that the companies were aware of significant supply chain problems or weaknesses, but failed to disclose them to the public.6 The SEC’s Division of Enforcement undoubtedly is investigating similar disclosures regarding supply chain issues.

Impacts of The Russia-Ukraine Conflict on the Supply Chain

In another widely publicized notice, the SEC has directed companies to evaluate their disclosures in light of Russia’s invasion of Ukraine. On May 2, 2022, CorpFin released a sample comment letter providing guidance on public reporting companies’ potential disclosure obligations. This guidance provided a variety of direct or indirect impacts the conflict might have on companies with operations or business ties to Russia, Ukraine, or Belarus. As related to supply chain disruptions, the SEC expressed its view that companies should provide detailed information concerning:

-

The “direct or indirect reliance on goods or services sourced in Russia or Ukraine or, in some cases, in countries supportive of Russia."7

-

The “actual or potential disruptions in the company’s supply chain."8

As the Russia-Ukraine conflict continues, companies with substantial operations outside of the United States and have referenced the Russia-Ukraine conflict in their filings have been asked by the SEC for more information. CorpFin has sought information in comment letters related to disclosures impacted by the Russia-Ukraine conflict, and has specifically requested information regarding “known trends or uncertainties” that have had or are reasonably likely to have a material impact on liquidity, financial position, or results of operations. As a result, issuers should pay close attention to the SEC’s guidelines and reflect any elevated risks or changes in its disclosures that are appropriate in light of the ongoing Russia-Ukraine conflict.

Climate-Related Risks to the Supply Chain

Another ongoing, and extremely controversial, area of interest for the SEC is climate-related disclosures. On March 21, 2022, the SEC released a proposed rule to standardize climate-related disclosures and add additional requirements to provide more information about climate-related risks.9 The rule broadly proposes disclosures regarding both actual and potential negative climate-related impacts on companies’ supply chains. It proposes disclosure requirements related to both “upstream” (the initial production activities) and “downstream” (the delivery of the product or service) activities of a company’s operations. These requirements call upon companies to look at the present and future risks of not just their direct operations, but the operations of other entities that may contribute to their production or delivery of products or services.

Although the proposed rule has faced fierce criticism from multiple constituencies in industry, government and media and is far from adoption, the SEC nonetheless is issuing comment letters relating to disclosure (or lack of disclosure) regarding climate change and supply chain issues in particular. Relying in large part on 2010 guidance regarding disclosures concerning climate change,10 CorpFin has inquired into weather-related events that have led to supply chain disruptions as well as climate-related regulatory changes that could impact operations through compliance burdens. Where companies have said in proposed filings that climate change impacts are not material, CorpFin is asking how this conclusion was reached.

With climate-related regulation in this country still in a formative state given the recent passage of the Inflation Reduction Act, it is difficult to predict with any certainty where such regulations will eventually land. Nonetheless, companies should start analyzing their climate-related risks with respect to their supply chains and their businesses more broadly.

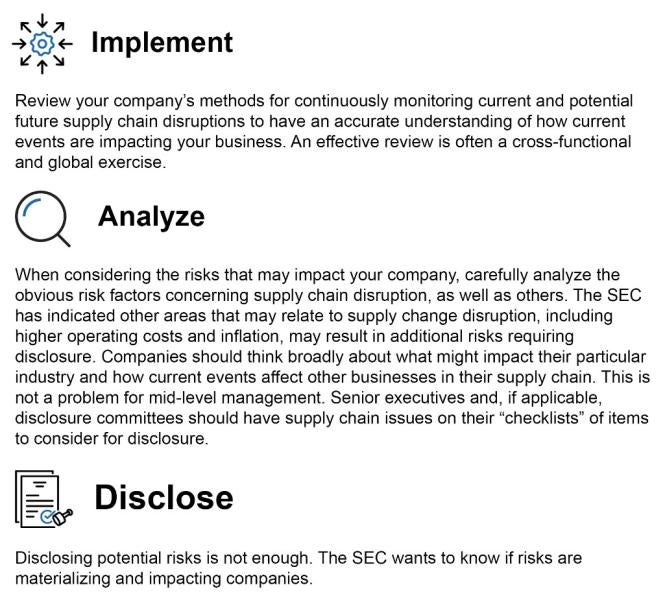

Key Takeaways - Reassessing Supply Chain Disclosure Best Practices

Current events have caused the SEC to issue unprecedented guidance regarding what disclosures are expected concerning a variety of impacts, including regarding supply chains. Although investors logically know supply chains are vital and subject to risk, the SEC is calling for more discussion on whether the risks are becoming a reality. Now is the time to reassess best practices with respect to potential disclosure regarding supply chain challenges:

FOOTNOTES

1 U.S. Securities and Exchange Commission, Coronavirus (COVID-19) CF Disclosure Guidance (March 25, 2020).

2 Id.

3 17 C.F.R. § 229.105.

4 17 C.F.R. § 229.303(b)(2)(ii).

5Interpretation: Commission Guidance Regarding Management’s Discussion and Analysis of Financial Condition and Results of Operations, Release Nos. 33-8350 and 34-48960.

6 LaCroix, Kevin, Supply Chain Disruption Leads to Securities Suit Against Mattress Manufacturer, The D&O Diary (December 15, 2021).

7 U.S. Securities and Exchange Commission, Sample Letter to Companies Regarding Disclosures Pertaining to Russia’s Invasion of Ukraine and Related Supply Chain Issues (May 3, 2022).

8 Id.

9 U.S. Securities and Exchange Commission, The Enhancement and Standardization of Climate-Related Disclosures for Investors (Mar. 21, 2022).

10 U.S. Securities and Exchange Commission, Commission Guidance Regarding Disclosure Related to Climate Change (Feb. 8, 2010).