/>i

/>iJULY – SEPTEMBER 2021: HIGHLIGHTS

UNITED STATES

-

The US Department of Justice’s (DOJ) challenge of American Airlines and JetBlue’s “Northeast Alliance” after the joint venture’s approval by the US Department of Transportation earlier this year demonstrates the Biden administration’s commitment to aggressive antitrust enforcement.

-

US President Joe Biden issued an Executive Order calling for tougher antitrust enforcement, including “encouraging” the DOJ and Federal Trade Commission (FTC) to modify the horizontal and vertical merger guidelines to address increasing consolidation. At the same time, the FTC, under Chair Lina Khan, continues its rapid pace of change to the merger review process, including introducing Pre-Consummation Warning Letters, rescinding the 2020 Vertical Merger Guidelines, repealing an over 25-year-old policy statement on “prior approval” obligations in merger settlements, and issuing more comprehensive and rigorous procedures for Second Requests. These changes only apply to transactions that the FTC reviews.

-

Aon PLC and Willis Towers Watson abandoned their tie-up following a DOJ challenge, and the FTC successfully obtained a preliminary injunction to prevent Hackensack Meridian Health from acquiring Englewood Healthcare, in major litigation wins for the antitrust agencies.

EUROPEAN UNION

-

Under a new interpretation of Article 22 of the EU Merger Regulation (EUMR), the European Commission (Commission) asserted jurisdiction over Illumina’s acquisition of GRAIL and Facebook’s acquisition of Kustomer, even though the transactions did not meet the Commission or Member State filing thresholds.

-

The EU’s Market Definition Notice will focus on innovation and digital markets.

-

The EU General Court confirms a significant gun-jumping fine imposed on Altice for breach of the EUMR notification and standstill obligations.

UNITED KINGDOM

-

The Competition & Markets Authority’s (CMA) handling of the Veolia/Suez transaction demonstrates the CMA’s willingness to engage with parties to seek practical interim solutions while it is investigating a consummated transaction for potential antitrust concerns.

-

The UK government published plans to update antitrust rules, including revising its jurisdictional thresholds and expanding the “share of supply” test to allow the CMA to more easily capture vertical and conglomerate mergers, as well as acquisitions of startups.

-

The CMA published its Annual Report 2020. In total, the CMA reviewed 600 transactions, with less than 5% of these prohibited or cleared subject to remedies.

KEY THEMES AND TAKEAWAYS

UNITED STATES

-

Sweeping Biden Executive Order Calls for Greater Antitrust Enforcement

On July 9, President Biden issued a wide-ranging Executive Order on Promoting Competition in the American Economy. The Order called for greater antitrust enforcement “to combat the excessive concentration of industry, the abuses of market power, and the harmful effects of monopoly and monopsony.” The Order also called for a special focus on labor markets, agricultural markets, internet platform industries and healthcare markets. The Order encourages antitrust agencies to enforce existing laws more vigorously, including reviewing and challenging consummated mergers that previous administrations did not challenge.

The Order specifically called out hospital consolidation, blaming “unchecked mergers” leading to “the ten largest healthcare systems now control[ling] a quarter of the market” and highlighted research showing higher hospital prices in consolidated markets. President Biden encouraged the antitrust agencies to review and revise merger guidelines to prevent patients from being harmed by such mergers. The Order also calls for greater scrutiny of acquisitions by large internet platforms, especially the acquisition of nascent competitors in order to eliminate a potential competitive threat.

-

FTC Warning Companies to Close Transactions “At Their Own Risk” Even After Expiration of HSR Waiting Period

In an August 3 blog post, then-acting Director of the FTC’s Bureau of Competition, Holly Vedova, announced that the FTC has begun sending Pre-Consummation Warning Letters cautioning merging companies that the FTC’s investigation of their transaction remains open after the expiration of the Hart-Scott Rodino (HSR) waiting period and the agency may subsequently determine that their deal is unlawful. The sample form letter explicitly states that “if the parties consummate this transaction before the Commission has completed its investigation, they [] do so at their own risk.”

In explaining the rationale for these letters, Vedova cited the “tidal wave” of merger filings impeding the FTC’s ability to fully investigate deals during the applicable statutory waiting period. Even though the issuance of such letters is new, the FTC has always had the authority to challenge consummated transactions, even those subject to pre-merger review under the HSR Act. The issuance of these letters has implications for parties’ negotiations of antitrust provisions in merger agreements, including whether the receipt of such a letter can be used to delay closing.

-

FTC Rescinds 2020 Vertical Merger Guidelines Citing “Unsound Economic Theories”

On September 15, the FTC voted 3-2 on party lines to repeal Vertical Merger Guidelines that it finalized with the DOJ just last year. The majority Commissioners’ statement specifically criticized the 2020 Vertical Merger Guidelines’ focus on efficiencies of vertical mergers, noting that the Clayton Act prohibits any merger that “may” substantially lessen competition and there is no statutory efficiencies defense. The majority specifically criticized the 2020 Guidelines’ citation of the elimination of double marginalization (EDM) as the principal reason to treat vertical mergers differently from horizontal mergers. The majority stated that EDM is not likely to occur absent very specific factual scenarios, and any such savings are unlikely to be passed on to consumers. DOJ, however, has not rescinded the Vertical Merger Guidelines, meaning that the two agencies may evaluate vertical mergers differently.

After the FTC vote, acting Assistant Attorney General Richard Powers stated that “the [DOJ] is conducting a careful review of the Horizontal Merger Guidelines and the Vertical Merger Guidelines to ensure they are appropriately skeptical of harmful mergers” and will work with the FTC to update the guidelines as appropriate.

-

FTC Announces Second Request Process Reforms

On September 28, Vedova (who was appointed Director of the FTC’s Bureau of Competition that same day) announced several changes to the FTC’s Second Request process. Requests will focus on “additional facets of market competition that may be impacted,” such as “how a proposed merger may affect labor markets, the cross-market effects of a transaction, and how the involvement of investment firms may affect market incentives to compete.” The FTC will also alter its procedures to require more upfront information about how a company maintains data and what e-discovery tools will be used to identify responsive materials. The FTC is also doing away with the option to submit partial privilege logs “which make it impossible to review the assertions of privilege that targets are making.”

-

Antitrust Agencies Successfully Challenge Mergers

On July 20, Berkshire Hathaway Energy and Dominion Energy abandoned their proposed natural gas pipeline transaction due to FTC concerns. See Notable Cases.

On July 26, insurance brokers Aon and Willis Towers Watson abandoned their merger in the face of a DOJ challenge. DOJ’s complaint alleged that the combination of the world’s second and third largest insurance brokers would reduce competition for American businesses in the administration of health and retirement benefits and managing complex risks, such as property and casualty insurance.

On August 4, a New Jersey federal court granted the FTC’s request for a preliminary injunction to block a merger between Hackensack Meridian Health and Englewood Healthcare. The FTC alleged that the transaction would give the combined entity control of three of the six general acute care hospitals in Bergen County, New Jersey. The win for the FTC comes after it lost its previous hospital challenge in December 2020, when a Pennsylvania federal judge refused to block the merger of Jefferson Health and Albert Einstein Healthcare Network. This was the FTC’s first loss on a hospital merger challenge going back several years. Hackensack and Englewood are appealing the lower court’s decision to the US Court of Appeals for the Third Circuit.

EUROPEAN UNION

-

The European Commission Asserts Jurisdiction in Illumina/GRAIL and Facebook/Kustomer

In March, the Commission published guidance on its future use of the referral mechanism set out in Article 22 of the EUMR. On August 2 and September 20, respectively, under Article 22, the Commission opened a Phase 2 in-depth investigation into Facebook’s acquisition of Kustomer and issued a Statement of Objections (SO) (i.e., a charge sheet) against Illumina for acquiring GRAIL without merger control clearance.

As to Facebook/Kustomer, the Commission raised concerns that the transaction may reduce competition in the market for the supply of customer relationship management (CRM) software and strengthen Facebook’s market position in the online display advertising market by increasing Facebook’s data-pool. The UK CMA investigated similar concerns, but ultimately cleared the transaction on September 27. See Notable Cases. It is possible that the Commission and the CMA may ultimately reach diverging conclusions regarding Facebook/Kustomer. In addition, after requesting the Commission review the transaction pursuant to Article 22 EUMR, the German Federal Cartel Office (FCO) launched an investigation to consider whether Facebook should have notified the transaction to the FCO. The transaction is rapidly turning into an example of the “whack-a-mole” merger control proceedings that practitioners had feared would result from the Commission’s Article 22 guidance.

As to Illumina/GRAIL, which was referred to the Commission by a number of EU Member States pursuant to Article 22 EUMR, the transaction is currently subject to an ongoing Phase 2 review. In August, however, Illumina announced that it had closed the transaction in order to comply with its obligations under the purchase agreement. As a result, the Commission opened a parallel gun-jumping investigation into Illumina’s alleged breach of the standstill obligation under the EUMR; if confirmed, this investigation could entail the imposition of a multimillion Euro fine on Illumina.

While the Commission’s SO focuses on Illumina’s closing of the transaction prior to receiving merger control clearance, the EU General Court (which is hearing a challenge as to whether the Commission has authority to review the transaction) will ultimately have to consider whether the Commission’s review of the transaction under Article 22 was legally sound in the first place, given that the transaction did not meet the Commission or Member State filing thresholds. The EU General Court’s judgment will hopefully provide clarity for companies when assessing the risks of a transaction which the Commission is reviewing pursuant to Article 22.

-

What Is and Isn’t Working: The Commission Publishes Its Evaluation of the EU Market Definition Notice (Notice)

On July 12, the Commission published a Staff Working Document evaluating the effectiveness of the current Notice, which informs the application of the EU antitrust rules in determining the relevant product market. The goal of the evaluation was to assess whether the Notice needs to be modified to address changes in how the Commission evaluates transactions, particularly in high-tech industries.

Although the Commission concluded that the basic principles of the Notice remain sound, it found that “the Notice does not fully cover recent evolutions in market definition practice, including those related to the digitalisation of the economy.” The Notice may therefore be revised to address perceived enforcement gaps brought about by the ever-increasing digitalization of markets. In particular, the evaluation demonstrated that a new revised Notice may incorporate the following elements: (i) companies will likely be subject to more wide-ranging document requests in M&A transactions and there will be a greater focus on econometrics; (ii) a revised SSNIP test (evaluating whether customers will switch to another product/service following a small but significant non-transitory increase in price) may be used; (iii) the Commission will also assess markets where products and services are marketed for “free” (particularly in digital “ecosystems”); (iv) the impact of globalization and import competition will play a greater role; and (v) non-price competition, including innovation will be increasingly factored into the assessment.

As a result, calculating market shares and reaching a clear conclusion on whether a transaction is problematic may become significantly more complicated for companies and their counsel. These conclusions should be factored into the assessment of the feasibility of a given transaction going forward.

-

EU General Court Confirms Altice “Jumped the Gun” in Its Acquisition of PT Portugal

On September 22, the EU General Court upheld the Commission’s decision to impose a fine of €124.5 million on Altice, (though it reduced the fine by €10 million) for infringing the notification and standstill obligations under the EUMR. The Court found that Altice, in the context of its acquisition of PT Portugal in 2014, not only had an ability to exercise decisive influence over PT Portugal but actually exercised that ability between signing and closing of the transaction. In particular:

-

Altice held a veto right over the termination/change of employment terms of PT Portugal’s management.

-

Changes to PT Portugal’s pricing policy required Altice’s consent.

-

As part of a new promotion campaign, Altice set targets for the campaign and PT Portugal sent regular updates to Altice on progress with respect thereto.

-

Altice could veto the conclusion, termination or modification of PT Portugal contracts with a threshold of €1 million (replacing a previous threshold of €5 million). This low threshold effectively meant that Altice was likely to be able to veto all PT Portugal contracts.

In addition, Altice attended regular meetings with PT Portugal, and PT Portugal informed Altice of its choice of suppliers. Altice also received access to PT Portugal’s competitively sensitive information, including margins, customers, future strategy and cost strategy. This was particularly problematic as Altice had subsidiaries that competed with PT Portugal.

The ability to influence “ordinary course” business decisions was decisive. The Court found, however, that Altice’s influence on decisions that were outside the ordinary course were permitted (e.g., Altice was able to block PT Portugal’s planned launch of a TV channel for dogs). Similarly, the Court held that, subject to proper protocols being in place (such as clean team agreements), pre-closing exchange of information was permitted as a necessary part of the due diligence process.

UNITED KINGDOM

-

The CMA’s Investigation into the Completed Acquisition of Suez by Veolia Does Not Need to Lead to a Complete Standstill

Veolia Environnement S.A. (Veolia) acquired a minority shareholding in Suez S.A. (Suez) and announced its plans to acquire the remaining shares in Suez through a public takeover bid. On February 1, however, the CMA issued an initial enforcement order (IEO) against Veolia concerning its initial acquisition of a 29.9% shareholding in Suez. An IEO requires parties subject to the order to put a halt to any integration. The CMA may grant a derogation from an IEO, however, to maintain the viability of the target business and/or limit it to what is necessary to prevent pre-emptive action.

Since the enforcement of the IEO, the CMA has granted 24 derogations in relation to the transaction, ranging from limiting the effect of the IEO to Veolia’s UK business (as it is a stand-alone-business), to joint activities undertaken in the ordinary course of business, appointing managers and terminating certain non-material contracts. While the CMA can grant derogations, they can also be revoked. In Veolia/Suez, the CMA became aware of facts (as part of its investigation into the transaction) that showed that Veolia and Suez’s interests had become aligned already after agreeing on the sale of Suez’s remaining shares and that such alignment of interests risked leading to illegal pre-emptive action. As a result, the CMA revoked several derogations to the stand-still obligation. While derogations themselves are not new, the number of derogations granted in this case highlights the CMA’s willingness to engage with parties and seek practical interim solutions while it is investigating a transaction for potential antitrust concerns.

Moreover, the CMA’s approach stands in stark contrast to the EU’s position on gun-jumping highlighted above in the summary of the EU General Court’s recent judgment against Altice.

-

The UK Merger Control Regime Should Focus on Ensuring Its Review of Problematic Deals Concludes More Swiftly

On July 20, the UK Government published plans to update the UK’s antitrust rules, including changes to the CMA’s jurisdictional thresholds.

While initial proposals included the introduction of mandatory notification requirements, the new proposals maintain the voluntary, non-suspensory regime has provided the CMA with significant flexibility to date. In fact, the proposals increase the revenue threshold from £70 million to £100 million and now exclude transactions where both parties have revenues of less than £10 million in the UK (thus reducing the number of notifiable transactions on the basis of turnover alone, but do not raise concerns). The proposals also expand the “share of supply” test by removing the need for an increment, thereby allowing the CMA to more easily capture vertical and conglomerate mergers, as well as acquisitions of startups.

In addition, the procedural rules are to be revised with a view to allowing parties to offer remedies earlier in Phase 2 proceedings (currently only available at the end of Phase 1 or after the CMA has published its provisional findings in Phase 2).

-

CMA Annual Report: Merger Control Statistics Highlight Its Focus on Problematic Deals

The CMA reviewed approximately 600 transactions, a large number of which were initiated by the CMA’s mergers intelligence unit. Of those 600, the CMA launched 38 Phase 1 investigations, nine Phase 2 investigations and concluded 12 cases. Ten transactions were abandoned or blocked, with a further eight cleared subject to remedies (together, less than 5% of all transactions reviewed).

Moreover, the report highlights that following Brexit, the CMA continues to review large-scale international deals that would have previously been subject to review under the EUMR alone (e.g., NVIDIA’s acquisition of Arm).

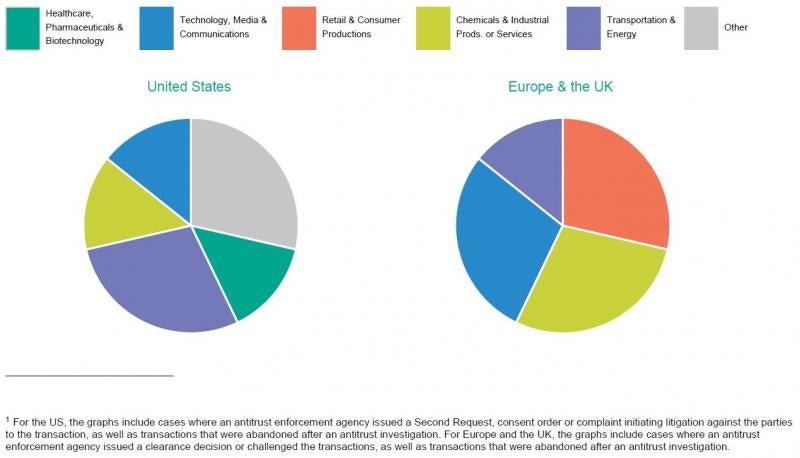

ENFORCEMENT IN KEY INDUSTRIES1

SNAPSHOT OF SELECTED ENFORCEMENT ACTIONS2

NOTABLE US CASES

| PARTIES | AGENCY | CASE TYPE (CLEARED, CONSENT, CHALLENGED, ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

| American Airlines (AA) / JetBlue | DOJ | Challenged | Air passenger service to/from Boston and New York City (NYC)

Alleged combined share ranging from 31% to 100% in various local markets |

On September 21, the DOJ and Attorneys General from six states and the District of Columbia filed a lawsuit seeking to unwind an alliance between AA and JetBlue. Notably, the action was brought under Section 1 of the Sherman Act. The DOJ alleged that a series of agreements between the airlines to share revenues and coordinate schedules (dubbed the “Northeast Alliance”) effectively consolidates the two airlines’ operations at four airports in Boston and NYC. According to the DOJ’s complaint, the “de-facto” merger in Boston and NYC will eliminate significant competition between the two airlines that results in lower fares and higher quality services for air travelers to/from these cities, and diminishes JetBlue’s incentives to compete with AA across the country.

The DOJ defined the relevant market as air passenger service between predetermined origins and destinations. The DOJ determined that the Northeast Alliance would be presumptively anticompetitive in 11 domestic markets where the two airlines provided (pre-pandemic) competing nonstop service to/from Boston, and 17 domestic markets where the two airlines provided competing nonstop service to/from NYC. The complaint also listed 98 additional markets that lack nonstop routes and where JetBlue’s connecting service through its Boston and NYC hubs competes with AA connecting service through its hubs. The DOJ alleged that the alliance will lower incentives for the two airlines to compete on these routes (as well because of the sharing revenues and capacity coordination on JetBlue’s service). The complaint also alleged that the alliance will harm competition in transatlantic markets, citing JetBlue’s previously announced plans to launch nonstop transatlantic service competing against AA between Boston/NYC and London. According to the complaint, because JetBlue will share in the revenues AA earns on its transatlantic routes (from Boston/NYC), it has less incentive to undercut American airlines on price. The DOJ’s complaint alleges that JetBlue is an important source of competition for AA, especially in the northeast, with an established reputation for lowering prices referred to in the industry as the “JetBlue effect.” Notably, the Trump administration’s Department of Transportation approved the alliance in January 2021, after securing commitments from the airlines to divest slots at two airports. |

| Gray Television / Quincy Media | DOJ | Consent | Two relevant product markets: (1) the licensing of “Big Four” television consent, and (2) the sale of broadcast television spot advertising

Geographic market for both: Designated Market Areas (DMA) |

On July 28, the DOJ reached a settlement with Gray Television Inc. (Gray) and Quincy Media Inc. (Quincy), requiring the divestiture of 10 broadcast television stations in seven local markets, to resolve concerns related to Gray’s proposed acquisition of Quincy.

The DOJ’s complaint alleged that Gray’s acquisition of Quincy would eliminate head-to-head competition between their broadcast television stations in seven local markets: Tucson, Arizona; Rockford, Illinois; Cedar Rapids, Iowa; Paducah, Kentucky; Eau Claire, Wisconsin; Madison, Wisconsin; and Wausau, Wisconsin. According to the complaint, the combined firm in these local markets would allegedly be able to charge cable and satellite companies higher retransmission fees to carry its broadcast stations, resulting in higher monthly bills for TV viewers. The combined firm would also allegedly be able to charge higher prices to businesses to advertise on its stations. Allen Media Holdings will acquire the 10 divested stations. |

| Berkshire Hathaway Energy / Dominion Energy | FTC | Abandoned | Transmission of natural gas from Rocky Mountain production basins to industrial customers in Central Utah

2-to-1 “merger to monopoly” |

On July 12, Dominion Energy (Dominion) and Berkshire Hathaway Energy, an affiliate of Berkshire Hathaway (Berkshire Hathaway), agreed to terminate an agreement that would have sold Dominion’s Questar Pipeline to Berkshire Hathaway. The parties abandoned the transaction following an FTC investigation.

The FTC’s press release following the parties’ announcement noted that its investigation revealed that Berkshire Hathaway’s Kern River Pipeline and Dominion’s Questar Pipeline are the only two pipelines that bring natural gas from the Rocky Mountain production basins to serve central Utah. In the press release, the FTC’s Vedova stated that it was “disappointing” that the FTC had to expend significant resources to investigate the transaction after the FTC previously sued to block the same transaction in 1995 and which the parties subsequently abandoned. Vedova further stated that this is the “type of transaction that should not make it out of the boardroom” and that the FTC “will be actively exploring its options on how to curtail this type of re-review to better deploy the Commission’s scarce resources.” Following the abandonment of the transaction, on July 21, the FTC voted 3-2 to rescind a 1995 policy statement that eliminated prior approval provisions from most merger settlements. Under the prior approval provisions, parties to a merger settlement are required to seek the approval of the Commission before engaging in a related transaction. FTC Chair Khan cited preserving the agency’s scarce resources as a primary rationale for this policy change. On October 25, the FTC formally reinstated its policy that merger settlements require acquiring companies to get prior Commission approval for any deal impacting “each relevant market for which a violation was alleged” for at least 10 years. |

NOTABLE EUROPEAN & UK CASES

| PARTIES | AGENCY | CASE TYPE (CLEARED, CONSENT, CHALLENGED, ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

| Aon / Willis Towers Watson | European Commission | Cleared Subject to Conditions (Phase 2) | Brokerage services to large multinational customers for various risks and re-insurance

3-to-2 |

The transaction was notified to the Commission on November 16, 2020, and cleared following a Phase 2 investigation with remedies on July 9, 2021.

The Commission considered the global presence of Aon and Willis Towers Watson to be of great importance when serving larger multinational customers in the management of their commercial risk. The Commission found that in the brokerage services market, aside from the Parties, only Marsh provided similar services. Similarly, with respect to re-insurance, the Commission considered the transaction a 3-to-2 merger. The Commission found that the commitment to divest central parts of Willis Towers Watson’s business to Arthur J Gallagher was sufficient to allay the Commission’s concerns. However, the parties later abandoned the transaction after the DOJ sued to block the transaction in the US. |

| viagogo / StubHub | CMA | Cleared Subject to Conditions (Phase 2) | Secondary ticketing, excluding classified ad sites, social media and primary ticketing

Alleged 90% market share in the UK |

On December 13, 2019, the CMA opened its investigation into viagogo’s acquisition of StubHub. The CMA ultimately cleared the transaction subject to remedies on September 8, 2021—nearly two years later.

After finding that the transaction would lead to a substantial lessening of competition in the secondary ticketing market in the UK, the CMA asked viagogo to sell all of StubHub’s business outside of North America. According to the CMA, only the sale of StubHub’s international business outside of North America was sufficient to ensure that customers in the UK had sufficient choice, as together the CMA found they held approximately 90% of the market). |

| Facebook / Kustomer | CMA | Phase 1 Clearance | Customer relationship management (CRM) software, business-to-consumer (B2C) messaging and online display advertising | On July 30, the CMA launched its investigation and ultimately cleared the transaction in Phase 1 on September 27.

The CMA concluded that it held jurisdiction because Facebook’s messaging channels and Kustomer’s proprietary webchat channel resulted in a share of supply of more than 25% in the UK. Even though the incremental increase in share brought about by the transaction was relatively small, the CMA noted this will always be the case in acquisitions of a nascent player. Conversely, the CMA considered that the size of Kustomer, even in the future, would not be such that the transaction would raise barriers to entry due to the small increase in data acquired, and most competitors could already access similar data. The CMA also considered potential vertical concerns, although it concluded that Facebook would not have an incentive to foreclose other CRM providers (as it benefits from the data generated by other CRM providers when using Facebook’s API). Similarly, other B2C messaging businesses would not lose the ability to compete simply due to a lack of Kustomer’s CRM. Finally, the CMA considered that the ability to offer Kustomer’s CRM software for free and subsidize its losses could reduce competition. That being said, the CMA found that competition would not be reduced to a significant extent due to the presence of other large international providers of CRM software. |