/>i

/>iOnce you have a business idea, creating a business entity may seem daunting from a legal standpoint.

However, setting up your business with thoughtful consideration and guidance will pay off over time, as you can structure your business to protect your personal assets, lessen your tax burden, and add legitimacy to your business. Each state has different requirements for business formations and annual filings, but the same general steps apply:

-

Pick a business name. Make sure the name isn't already in use by going to the Secretary of State website for the state where you plan to incorporate and run a simple business search. In many states, this search is free, but in some states, there may be a small charge.

-

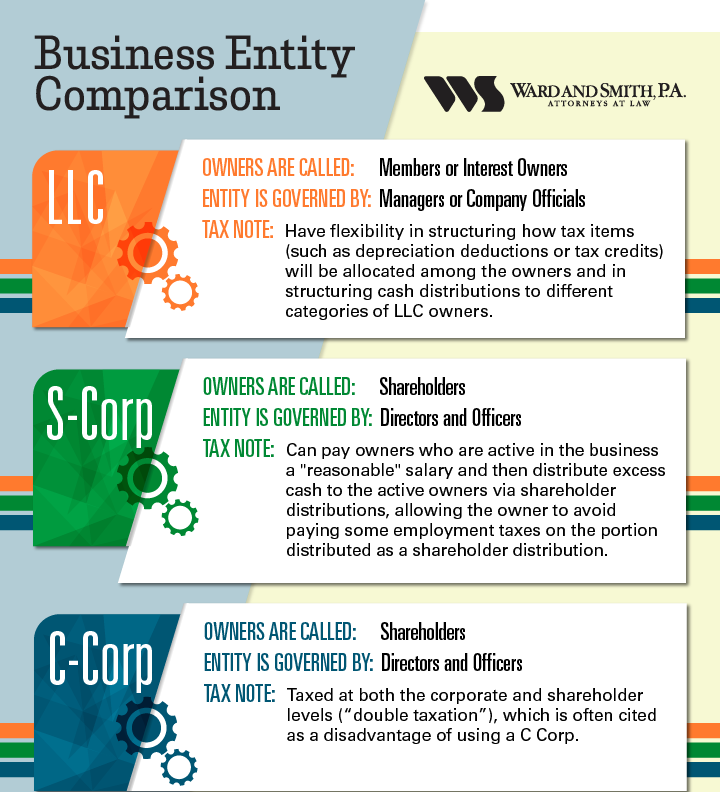

Decide which business entity to use. At this stage, consider consulting a business lawyer or accountant to discuss the tax implications of each entity type and receive personalized advice. You will ideally choose the business entity that maximizes the protection of your personal assets while minimizing your tax burden. Most closely held businesses should be formed as either a limited liability company ("LLC") or a Subchapter S Corporation ("S Corp"), although some may also be formed as a C Corporation ("C Corp"). While you can operate a business individually as a sole proprietor, which is the automatic status that comes from not formally setting up a business entity at all, you can be held personally liable for the debts and obligations of the business. Some general differences and considerations for LLCs, S Corps, and C Corps are:

-

Register your business with the Secretary of State. To create an LLC, you will file "Articles of Organization." To create an S Corp or C Corp, you will file "Articles of Incorporation." The state of formation can be the location where the business has its headquarters, or it can be another state as long as the business maintains a registered agent there. For most closely held businesses, the simplest and most logical place to register is in your own state.

-

Many states allow you to create an online account to submit your filing and create new filings later if needed. Once the Secretary of State files your filing, the filing will list the date that your entity officially came into existence.

-

-

Prepare an Operating Agreement or Bylaws. An LLC has an "Operating Agreement," while an S Corp or C Corp has "Bylaws." Both documents govern the internal affairs of the business, such as how often meetings will take place and how records will be kept. You will keep this document in your corporate records, but you do not need to file it with the Secretary of State. Note that you will want to include provisions regarding corporate governance, transfer rights, and other items in an Operating Agreement or Shareholders' Agreement if there are multiple owners of your new business.

-

Apply for an Employer Identification Number (EIN) online with the IRS. An EIN is the business equivalent to a Social Security Number, and you will use it to file your business taxes and open a business bank account. The EIN filing, which can be done online via the IRS's website, is relatively quick and painless if you have completed the above steps, and you will receive an EIN immediately at the end.

-

For an S Corp only: file Form 2553 with the IRS. To elect S Corp tax status, you'll need to file this form no later than two months, and 15 days after the beginning of the tax year the S Corp election will take effect or at any time during the tax year preceding the tax year the S Corp election will take effect.

-

Open a business bank account. To maintain your limited personal liability, you should keep business funds separate from your personal funds. If your bank requires setting up the account in person, call in advance to make sure you bring any documents the bank requires, in addition to the EIN.

-

Make a plan for your business finances and taxes. Just like personal income taxes, businesses have to pay taxes at both the state and federal levels. Note that even pass-through entities, such as LLCs and S corps will owe certain taxes, such as sales taxes and employment taxes, even though the entity itself does not pay income taxes. You may wish to schedule a meeting with an accountant at this point. Some practical suggestions to keep track of finances and taxes include:

-

Making a list that contains all financial-related tasks that happen monthly, such as running payroll, which can include paying yourself.

-

Creating a month-by-month list of deadlines that occur quarterly or yearly, such as paying quarterly taxes and filing an annual report with the Secretary of State where your business is incorporated.

-

Discussing with an accountant what business expenses may be tax-deductible, so you can keep a clear record of deductible expenses long before tax season comes around.

-

Investing in a payroll and/or accounting software. Many of these platforms will run payroll with just a few clicks of a mouse, provide payroll and tax reports that you can easily supply to an accountant, and even file quarterly taxes for you, freeing you up to focus on growing your business.

-

-

Apply for any necessary licenses, permits, or certificates specific to your industry. Businesses in certain industries must have permits or certificates in place to be authorized to do business in the particular industry. For example, restaurants may be required to obtain a business license, certificate of occupancy, food service license, sign permit, liquor license, and more.

-

Research and obtain the proper insurance coverage for your business and industry, as applicable. You can work with a trusted insurance broker to put together a customized plan that works for your business.

With these steps complete, your business will be off to a great start!