/>i

/>iOn November 21, 2019, the Federal Energy Regulatory Commission (FERC or Commission) issued Opinion No. 569, setting forth a new methodology for: (i) determining whether an existing return on equity (ROE) has become unjust and unreasonable under Section 206 of the Federal Power Act (FPA); and (ii) establishing a just and reasonable ROE for public utilities. Most importantly, FERC explained that it would rely on the discounted cash flow (DCF) model and the Capital Assets Pricing Model (CAPM), but not other cost of equity models.

Background

The Commission has been considering changes to its method of determining ROE for electric utilities since issuing Opinion No. 531 in 2014, when it decided to apply a “two-step” DCF methodology, incorporating long-term growth projections, in evaluating ROE for the transmission owners in New England. The U.S. Court of Appeals for the D.C. Circuit vacated and remanded this decision in Emera Maine v. FERC, leading the Commission to propose to a new approach to ROE evaluation in a case involving the New England transmission owners, and in separate complaint proceedings concerning the ROEs of the transmission owners in the Midcontinent ISO (MISO). In these so-called “Briefing Orders,” the Commission proposed to give equal weight in its ROE computations to four financial models—DCF, CAPM, Expected Earnings, and Risk Premium—and ordered the participants to submit briefs addressing the proposed changes.

FERC’s New Methodology for Evaluating Return on Equity

Cost of Equity Analysis

In Opinion No. 569, the Commission decided not to incorporate consideration of the Expected Earnings and Risk Premium approaches, and instead determined to evaluate ROE using only the DCF and CAPM models. The Commission found that the DCF and CAPM methods are the methods that investors use most commonly to estimate the cost of equity, and decided not to use the Expected Earnings and Risk Premium models in light of their complexities and potential inaccuracies. The Commission’s new approach involves evaluating cost of equity for each utility in a proxy group using both the DCF and CAPM models, eliminating outliers, and then averaging the high values and low values determined using the DCF and CAPM models to establish the endpoints.

The Commission also made calls on a number of other details of how ROE analysis is to be done, including:

-

In the DCF analysis, FERC will continue to use a two-step DCF analysis that incorporates a long-term growth rate based on GDP, will use the short-term growth rate to adjust dividend yield, and, “absent compelling reasons,” will use only the Institutional Brokers’ Estimate System (IBES) as the source of short-term earnings growth estimates;

-

In the CAPM analysis, FERC will use a forward-looking approach, use a one-step DCF (without a long-term growth rate) for the DCF analysis within the CAPM, use only IBES as the source of short-term earnings growth estimates for the DCF analysis within the CAPM, screen from the CAPM analysis S&P 500 companies with growth rates that are negative or greater than 20 percent, and include a size-premium adjustment;

-

Low-end outliers will be dropped if ROE results are below yields of Baa bonds plus 20 percent of the CAPM risk premium; and

-

FERC will continue to use the midpoint as the central tendency for analysis of ROE for groups of utilities.

Evaluation of an Existing ROE under Section 206 of the Federal Power Act

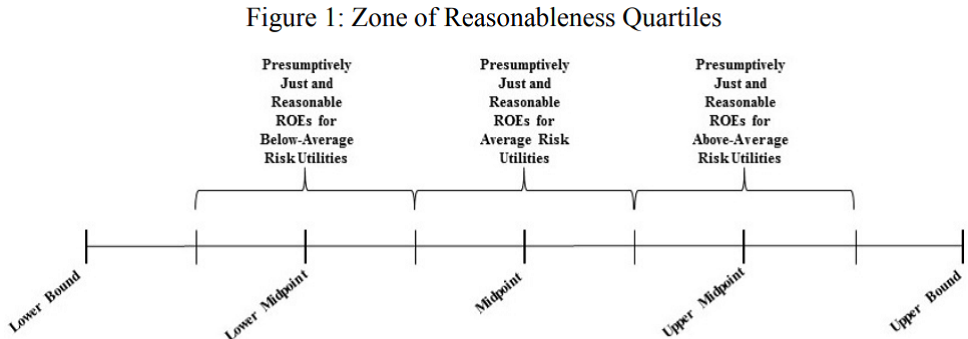

To determine whether an existing ROE has become unjust and unreasonable, the Commission will establish a zone of reasonableness reflecting the current market cost of equity based on the composite zones of reasonableness found by the DCF and CAPM methods, giving equal weight to the two models. In evaluating the ROE applicable to a group of utilities, such as the MISO utilities, the Commission will then determine the midpoint, the midpoint of the upper end, and the midpoint of the lower end, and use the quartiles around each of these three points to evaluate the current ROE, depending on the utilities’ relative risk. The Commission determined to break utilities into three categories of risk: average, below-average, and above-average. For average-risk utilities, the presumptively just and reasonable range is the quartile of the overall composite zone of reasonableness centered on the central tendency of the overall zone of reasonable. For below- and above-average risk utilities, respectively, the presumptively just and reasonable ranges are the quartiles centered on the central tendencies of the lower and upper halves of the zone of reasonableness. The Commission provided the following illustration of these quartiles:

The Commission explained, however, that these presumptions can be rebutted by other evidence, “such as evidence regarding non-utility stock prices, investor expectations for non-utility stocks, various types of bond yields and their relation to stock prices, investor and other expert testimony, and testimony regarding the effects of rates on customers.”

Establishment of a New Base ROE

To determine a new just and reasonable ROE under the second prong of FPA Section 206 (and under FPA Section 205), the Commission decided to use the central tendency of the overall composite zone of reasonableness for average risk utilities, the central tendency of the upper half of the composite zone of reasonableness for above-average risk utilities, and the central tendency of the lower half of the composite zone of reasonableness for below-average risk utilities. The order provides little express direction on how to determine a utility’s appropriate risk category. The Commission noted that it would not foreclose the possibility that a particular utility could be of such high or low risk to justify setting its ROE at the top or bottom of the composite zone of reasonableness.

Application to the MISO Transmission Owners

Opinion No. 569 addressed two separate complaints—filed 15 months apart—challenging the MISO transmission owners’ ROE. The first complaint was filed on November 13, 2013, challenging the MISO transmission owners’ then-existing base ROE of 12.38 percent. The Commission set a refund period from November 13, 2013 through February 12, 2015. While the first complaint remained pending, a second complaint was filed on February 12, 2015, challenging the 12.38 percent base ROE. The Commission set the second complaint for hearing and established a refund period from February 12, 2015 to May 11, 2016. On September 28, 2016, the Commission issued Opinion No. 551 in the first complaint proceeding, finding the MISO transmission owners’ existing ROE to be unjust and unreasonable, and ordering the MISO transmission owners to set a base ROE of 10.32 percent as of that date. The Commission ordered the issuance of refunds for the 15-month refund period following the date the first complaint was filed in November 2013.

In Opinion No. 569, the Commission granted rehearing of its order on the first complaint. Using data from the first six months of 2015, the Commission found that the composite zone of reasonableness using the DCF and CAPM methods was 7.52 percent to 12.24 percent, with a midpoint of 9.88 percent. The Commission found that the MISO transmission owners were of average risk, and thus compared their base ROE to the quartile centered on the midpoint of the zone of reasonableness. That quartile was between 9.29 percent and 10.47 percent. On this basis, the Commission found the MISO transmission owners’ base ROE of 12.38 percent to be unjust and unreasonable, and ordered the establishment of a base ROE of 9.88 percent effective September 28, 2016— the date the Commission had previously required the MISO transmission owners to revise their ROEs in Opinion No. 551. The Commission ordered the MISO transmission owners to provide refunds, with interest, for the 15-month period from November 12, 2013 through February 11, 2015.

Addressing the second complaint, the Commission considered the 9.88 percent base ROE that was established as of September 28, 2016 under the first complaint, using data from the six-month period from July 2015 to December 2015. The Commission found that the composite zone of reasonableness for this period was about the same as it was under the first complaint, so a base ROE of 9.88 percent remained just and reasonable.

Refunds in the Second Complaint Proceeding

Because the Commission determined that the 9.88 percent base ROE evaluated under the second complaint was just and reasonable, the Commission declined to order refunds for the 15-month period following the filing of the second complaint, despite the fact that the base ROE actually in effect during that period was 12.38 percent. The Commission explained that FPA Section 206 only permits it to order refunds in a complaint proceeding when the Commission grants prospective relief in that proceeding. The Commission reasoned that because it evaluated the second complaint in light of the 9.88 percent ROE that it found to be just and reasonable, it did not order prospective relief in that proceeding and thus was not permitted to order refunds. Commissioner Glick dissented on this determination, stating that he believes it would deprive customers of the full refund protections intended by the FPA.

Implications

The new methodology announced in Order No. 569 for use in electric utility ROE determinations is the latest action in an area that has been in flux for the past five years. Key issues and implications include:

-

The ROEs produced using both the DCF and CAPM models are, at least in current circumstances, higher than those produced by the DCF model alone, but lower than the four-model approach proposed in 2018.

-

FERC will continue to use the midpoint as the “central tendency” for ROE analyses of a group of public utilities (such as the MISO transmission owners), and the median as the central tendency for a single utility. The median has generally been lower than the midpoint in recent analyses.

-

The order addresses the application of ROE analysis to FPA Section 206 cases. It also states that the analysis in Section 205 cases will follow that used in the second step of the Section 206 analysis.

-

The order does not address the question of whether the same methodology will now be used for ROE determinations in natural gas and oil pipeline ratemaking proceedings.

FERC issued and received comments on a Notice of Inquiry Regarding the Commission’s Policy for Determining Return on Equity earlier this year. Issues left unresolved in Order No. 569 could be addressed in subsequent cases, or in a generic policy building on the record established in that NOI proceeding.