/>i

/>iOn October 26, 2011, the Securities and Exchange Commission (the “SEC”) adopted Rule 204(b)‑1 under the Investment Advisers Act of 1940 (the “Advisers Act”) to require certain investment advisers that advise private funds to periodically complete and file the SEC’s new Form PF.1 Rule 204(b)-1 implements sections 404 and 406 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) and is intended to provide the SEC with information relevant to assessing the risks that certain advisers and funds pose to the stability of the financial system. Although Form PF is filed confidentially and exempt from the Freedom of Information Act, the SEC is permitted to share this information with other federal agencies (most notably the Commodity Futures Trading Commission and the Financial Stability Oversight Council).

The requirements of the rule and Form PF are novel and the amount of information required to be assembled can be—at least in certain instances—quite substantial. With the initial compliance dates for investment advisers to certain large private funds approaching in June 2012, now is the time for investment advisers to become familiar with this new regulatory requirement, to determine when their initial Form PF filing will be due, and to identify and begin to assemble the types and extent of the information that will be required.

The full text of the adopting release and the final rule is available here. The full text of Form PF is available here.

What Investment Advisers Are Subject to Rule 204(b)-1 and Must File Form PF?

The new rule requires any investment adviser registered (or required to register) with the SEC under the Advisers Act that advises one or more “private funds” and has, in aggregate, $150 million or more in private fund assets under management to file Form PF. For purposes of determining whether they meet certain regulatory thresholds established by Form PF, related advisers must aggregate their assets under management; however, related advisers do not need to aggregate their assets if they are “separately operated.”2

What is a “Private Fund”?

The term “private fund” is defined in Section 202(a)(29) of the Advisers Act as any issuer “that would be an investment company,” as defined in the Investment Company Act of 1940, as amended (the “ICA”), but is excepted by virtue of the exemptions provided in Section 3(c)(1) (funds with fewer than 100 beneficial owners) or Section 3(c)(7) (funds owned exclusively by qualified purchasers) of the ICA. Real estate funds relying on the exemption provided in Section 3(c)(5) of the ICA are not required to file Form PF (although many real estate funds, because of the nature and structure of their investments, rely on the exemptions provided under Section 3(c)(1) or (7) and therefore may be required to file).

Form PF establishes different treatment—in terms of initial filing dates, the frequency of filings and the content of those filings—based on the characteristics of the private funds involved and their advisers. The most important distinction that Form PF draws in this regard is between “Large Private Fund Advisers” and all other investment advisers to private funds.

What is a “Large Private Fund Adviser”?

A “Large Private Fund Adviser” is defined as a private fund adviser that meets any one or more of the following criteria:

- it has at least $1.5 billion in regulatory assets under management attributable to hedge funds as of the end of any month in the most recently completed fiscal quarter;

- it has at least $1.0 billion in combined regulatory assets under management attributable to liquidity funds and registered money market funds3 as of the end of any month in the most recently completed fiscal quarter; and/or

- it has at least $2.0 billion in regulatory assets under management attributable to private equity funds as of the last day of the adviser’s most recently completed fiscal year.

How are Regulatory Assets Under Management Calculated?

The term “regulatory assets under management” has the same meaning given to it in the SEC’s recent amendments to Part 1A, Instruction 5.b of Form ADV. This definition measures assets under management gross of outstanding indebtedness and other accrued but unpaid liabilities.

In addition, in order to prevent an adviser from restructuring the way it manages money to avoid compliance with Form PF, the rule requires regulatory assets under management to include (a) assets of managed accounts advised by the adviser that pursue substantially the same investment objective and invest in substantially the same positions as private funds advised by the firm unless the value of those accounts exceeds the value of the private funds with which they are managed; and/or (b) assets of private funds advised by any of the adviser’s “related persons” other than related persons that are separately operated.

What is a “Hedge Fund”?

Form PF defines a “hedge fund” as any private fund that is not a securitized asset fund4 if it meets any of the three following criteria:

- it is permitted to pay one or more investment advisers (or their related persons) a performance fee or allocation calculated by taking into account unrealized gains;

- it is permitted to borrow an amount in excess of one-half of its net asset value (including any committed capital); and/or

- it is permitted to sell securities or other assets short or enter into similar transactions (other than for the purpose of hedging currency exposure or managing duration).

Note that for purposes of the first criteria above, the fund must only be authorized to pay a fee based on unrealized gains (the classification applies whether or not the performance fee is actually paid). In the Adopting Release, the SEC clarified that the periodic calculation or accrual of performance fees based on unrealized gains solely for financial reporting purposes (as many private equity funds do) will not cause a private fund to be classified as a hedge fund. For purposes of the second and third criteria cited above, the private fund must be authorized to undertake such activities; actually undertaking the activities is not required.5

What is a “Liquidity Fund”?

Form PF defines a “liquidity fund” as any private fund “that seeks to generate income by investing in a portfolio of short term obligations in order to maintain a stable net asset value per unit or minimize principal volatility for investors.” Thus, a liquidity fund would be a private fund that resembles a registered money market fund.

What is a “Private Equity Fund”?

Form PF defines a “private equity fund” as any private fund that is not a hedge fund, liquidity fund, securitized asset fund, real estate fund,6 or venture capital fund7 and does not provide investors with a right to redeem their interests in the ordinary course.

Does the SEC’s Focus on Hedge Funds, Liquidity Funds and Private Equity Funds Mean that Other Types of Private Funds are Not Subject to Rule 204(b)(1) and Form PF?

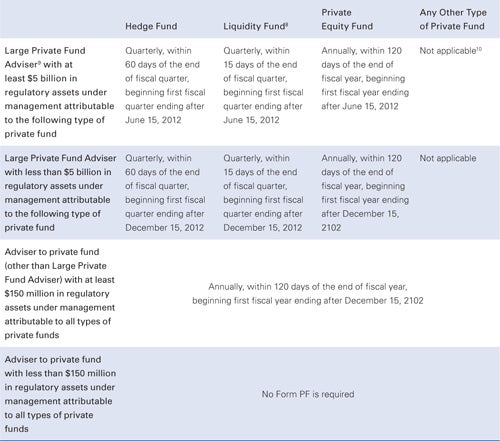

No. As the charts below show, an investment adviser that is not a Large Private Fund Adviser and that does not advise any hedge funds, liquidity funds or private equity funds must still prepare and file Form PF if it advises private funds with $150 million or more in private fund assets.

What are the Initial Compliance Dates for Form PF?

Form PF and Rule 204(b)-1 establish June 15, 2012 as the initial “compliance date” for any registered investment adviser (or an adviser that is required to register) that meets one or more of the following criteria:

- it has at least $5.0 billion in regulatory assets under management attributable to hedge funds as of the last day of its fiscal quarter most recently completed prior to June 15, 2012;

- it has at least $5.0 billion in combined regulatory assets under management attributable to liquidity funds and registered money market funds as of the last day of its fiscal quarter most recently completed prior to June 15, 2012; and/or

- it has at least $5.0 billion in regulatory assets under management attributable to private equity funds as of the last day of its first fiscal year to end on or after June 15, 2012.

An adviser subject to the June 15, 2012 compliance date as a result of its advice to hedge funds and/or liquidity funds/money market funds will need to file its initial Form PF for the first fiscal quarter ending after June 15, 2012. For most such advisers, this will be for the fiscal quarter ending June 30, 2012 (and will be due August 29, 2012 for hedge fund advisers and July 15, 2012 for liquidity fund advisers). An adviser subject to the June 15, 2012 compliance date as a result of its advice to private equity funds will need to file its initial Form PF for the first fiscal year ending after June 15, 2012. For most such advisers, this will be for the fiscal year ending December 31, 2012 (and will be due April 30, 2013).

For all investment advisers that are not subject to the June 15, 2012 compliance date, the compliance date will be December 15, 2012. However, whether such advisers will be filing with respect to the first fiscal quarter or first fiscal year ending after that date (and the deadline for such filing) will depend on the type of private funds advised and the amount of assets under management as set forth in Table I below.

TABLE I

Regulatory assets under management for the fiscal quarter or year (as the case may be) ending immediately after June 15, 2012 are, for hedge funds and liquidity funds, measured as of the last day of the fiscal quarter ending immediately prior to such date, and for private equity funds measured, as of the last day of the fiscal year ending immediately prior to such date. For any other Form PF filing under Rule 204(b)-1, regulatory assets under management, for quarterly Form PF filers, are measured as of the end of each month in the immediately preceding fiscal quarter (and the threshold is passed if, as of any month end, the assets under management exceed the relevant threshold), and, for annual Form PF filers, are measured solely as of the last day of the immediately preceding fiscal year.

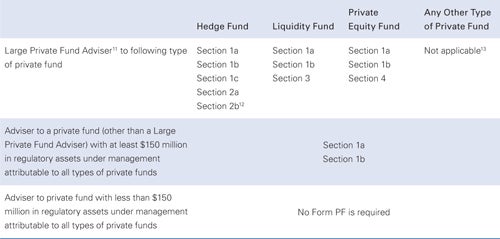

What Type of Information Must Be Included in the Form PF?

As with other issues under the new Form PF, the answer to this question depends on the size and nature of the private funds advised. Investment advisers to private funds (other than Large Private Fund Advisers) have much more limited disclosure obligations than Large Private Fund Advisers. In addition, as it relates to Large Private Fund Advisers, the additional disclosures required have been tailored to whether the private fund advised is a hedge fund, liquidity fund or private equity fund. Table II below summarizes the information requirements imposed by Form PF.

TABLE II

Investment Advisers should start now to determine whether they will be required to file the new Form PF, to determine the applicable filing date for any form PF filing, and to identify and begin to assemble the required information necessary to complete the form.

1. See Reporting by Investment Advisers to Private Funds and Certain Commodity Pool Operators and Commodity Trading Advisors on Form PF, Release No. IA-3308; File No. S7-05-11 (October 31, 2011) (the “Adopting Release”).

2. An adviser is not required to aggregate its private fund assets with those of a related person if the adviser is not required to complete Section 7.A of Schedule D to its Form ADV with respect to such related person. The criteria for excluding a related person from Section 7.A of Schedule D to an adviser’s Form ADV include (i) the adviser having no business dealings with the related person in connection with advisory services provided to its clients; (ii) the adviser not conducting shared operations with the related person; (iii) the adviser not referring clients or business to the related person, and the related person not referring prospective clients or business to the adviser; (iv) the adviser not sharing supervised persons or premises with the related person; and (v) the adviser having no reason to believe that its relationship with the related person otherwise creates a conflict of interest with its clients.

3. An adviser that manages liquidity funds and registered money market funds must combine the assets in those funds for purposes of determining whether it qualifies as a Large Private Fund Adviser.

4. A securitized asset fund is a private fund whose main purpose is to issue asset backed debt securities.

5. This test does not require that the fund’s organizational documents expressly prohibit such leverage or short-selling as long as “the fund in fact does not engage in these practices … and a reasonable investor would understand, based on the fund’s offering documents, that the fund will not engage in these practices.” See Adopting Release at page 28.

6. A real estate fund is defined as a private fund that invests primarily in real estate and real estate-related assets as long as it is not a hedge fund and does not provide investors the right to redeem in the ordinary course.

7. A venture capital fund is defined by reference to Rule 203(l)-1 of the Advisers Act. That rule is complex, subject to various exceptions, definitions and other discussions, and easily could be the subject of its own client alert. In short, a venture capital fund is defined as a private fund that: (i) holds no more than 20 percent of the fund’s capital commitments in certain non-qualifying investments; (ii) does not incur leverage, other than limited short-term borrowing; (iii) does not offer its investors a right to redeem except in extraordinary circumstances; (iv) represents itself as pursuing a venture capital strategy; and (v) is not registered as a business development company.

8. For purposes of calculating the amount of regulatory assets under management by a manager to a liquidity fund, regulatory assets under management include the combined assets under management attributable to all liquidity funds and registered money market funds.

9. A “Large Private Fund Adviser” includes (i) any adviser that has at least $1.5 billion in regulatory assets under management attributable to hedge funds, (ii) any adviser that has at least $1.0 billion in regulatory assets under management attributable to liquidity funds and registered money market funds, or (iii) any adviser that has more than $2.0 billion in regulatory assets under management attributable to private equity funds.

10. An adviser solely to private funds other than hedge, liquidity and private equity funds would not be a Large Private Fund Adviser regardless of the assets under management in those funds.

11. See Note 9.

12. Form PF requires additional disclosures in Section 2b by Large Private Fund Advisers with respect to any hedge fund that has a net asset value of at least $500 million.

13. See Note 10.