/>i

/>iOn December 1, 2020, Nasdaq filed with the Securities and Exchange Commission (SEC) a proposal to adopt new listing rules related to board diversity. If approved, the new listing rules would require Nasdaq-listed companies, subject to certain exceptions, to (1) have, or explain why they do not have, at least two diverse directors, and (2) to provide statistical information on the company’s board of directors related to a director’s self-identified gender, race and self-identification as LGBTQ+. Nasdaq stated that the goal of the proposed listing rules is to provide stakeholders with a better understanding of a company’s current board composition and enhance investor confidence that Nasdaq-listed companies are considering diversity in the context of selecting directors.

The proposal will be open for a public comment period of a minimum of 21 days from the time the proposed rules are published in the Federal Register. After publication in the Federal Register, the SEC will have 30 to 240 calendar days to review and approve the rule proposal.

Diverse Board Representation

Board Composition Requirements

The proposed rules would require each Nasdaq-listed company to either (1) have at least two diverse directors, including one director who self-identifies as female and one director who self-identifies as an underrepresented minority or LGBTQ+, or (2) disclose in the proxy statement or information statement for its annual meeting of shareholders, or on its website, that the Nasdaq requirement applies to the company, and provide an explanation of why the company does not have the requisite number of diverse directors. If the company provided such disclosure on its website, it would be required to also notify Nasdaq of the location where the information was available by submitting the URL link through the Nasdaq Listing Center no later than 15 calendar days after its annual shareholder meeting.

Smaller reporting companies would be permitted to satisfy the board composition requirement by having two female directors, rather than one female director and one director who self-identifies as either an underrepresented minority or LGBTQ+. If a company chose to satisfy the requirement by explaining why it did not have two diverse directors, Nasdaq would not assess the substance of the company’s explanation but would verify that the company had provided one.

The proposed rules define “diverse” as including individuals who self-identify as female, as an underrepresented minority or as LGBTQ+.

-

“Female” is defined as an individual who self-identifies her gender as a woman, without regard to the individual’s designated sex at birth.

-

“Underrepresented minority” is defined as an individual who self-identifies as one or more of the following: Black or African American, Hispanic or Latinx, Asian, Native American or Alaska Native, Native Hawaiian or Pacific Islander, or two or more races or ethnicities.

-

“LGBTQ+” is defined as an individual who self-identifies as lesbian, gay, bisexual, transgender or as a member of the queer community.

Phase-In Periods

Under the proposed rules, each Nasdaq-listed company would be required to have, or explain why it does not have, at least one diverse director no later than two calendar years after the date of SEC approval of the proposed rules. Companies listed on the Nasdaq Global Select Market or Global Market tiers would be required to have at least two diverse directors no later than four calendar years after the approval date, while companies listed on the Nasdaq Capital Market tier would be required to have at least two diverse directors no later than five calendar years after the approval date.

After the four- or five-year phase-in period expires, newly-listed companies, including IPOs, direct listings and SPAC listings in connection with business combinations, would have one year from the date of listing to satisfy the diversity requirement. Companies listing before the expiration of the phase-in period would have the remainder of phase-in period or one year from the date of listing, whichever is longer, to satisfy the requirement.

If a company did not have at least two diverse directors and failed provide the necessary disclosure, Nasdaq would notify the company that it was not in compliance with a listing requirement. The company would have until the latter of its next annual shareholder meeting or 180 days from the event that caused the deficiency to cure the deficiency. If the company did not regain compliance within the applicable cure period, it could be subject to delisting.

Board Diversity Disclosure

Board Statistical Disclosure Requirements

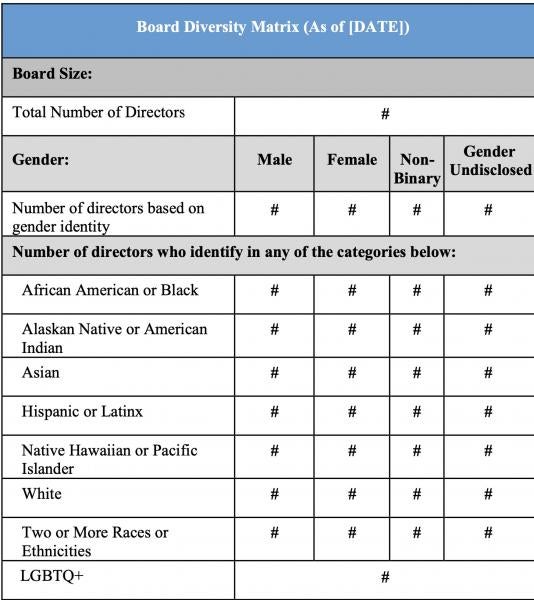

Under the proposed rules, Nasdaq-listed companies would be required to publicly disclose, on an annual basis, diversity statistics regarding their boards of directors. Companies would be required to provide this disclosure in either the proxy statement or information statement for their annual meetings of shareholders, or on their website. If a company elected to post the disclosure on its website, it would also need to submit such disclosure along with a URL link to the information through the Nasdaq Listing Center within 15 calendar days of the company’s annual shareholder meeting.

Each company would be required to provide its board-level diversity data in a format substantially similar to the example Board Diversity Matrix included in the proposal.

Phase-In Period

The initial disclosure under this listing requirement would be required within one calendar year of the SEC’s approval of the proposed listing rules. For the first year a company was required to disclose board diversity statistics, the company would be required to publish board diversity statistics for that year only. Each subsequent year, the company would be required to publish its data for each of the last two years. Nasdaq believes that disclosing at least two years of data allows the public to view any changes and track a board’s diversity progress.