/>i

/>iThe payment and withholding of earned income taxes (“EIT taxes”) in the Commonwealth of Pennsylvania at times seems like a complex maze and is challenging for human resource professionals or a company’s payroll tax team. In May of 2018,[1 Pennsylvania amended its Local Tax Enabling Act.[2] Most Pennsylvania municipalities levy an earned income tax on their residents at the rate of 1%. Nearly all municipalities also have a “non-resident” EIT tax rate, which is the same or higher than the rate for “residents.”[3] Some distressed municipalities have a higher EIT Tax rate, resulting in the division of withholding taxes between the employee’s resident municipality and the workplace municipality.

The following is a guide for employers on the proper withholding of municipal earned income taxes (“EIT Taxes”) for employees working out of a location where the work location EIT tax is greater than 1%. However, this guide will apply to any political subdivision in which the employer is located. For purposes of illustration in this guide, the employer is located in the hypothetical “Example City” that has a work location EIT tax of 1.4%.[4]

-

Residency Certification Forms. All employers in Pennsylvania must complete a Residency Certification Form for each of its employees in order to compare the employees’ “Total Resident EIT Rate” for the municipality where the employee resides with the “Work Location Non-Resident EIT Rate” for the municipality in which the employee works. At times, both EIT rates will be identical either (a) because the employee is domiciled in the same political subdivision that he or she works, or (b) because the EIT rates for both political subdivisions are the same. This form can be found online at: https://www.hab-inc.com/wpcontent/uploads/Residency-Certification-Form-DCED-CLGS-32-6-8-11.pdf. This form must be signed by the employee who certifies his resident municipality is correct. Employers are permitted to rely on their certification.

-

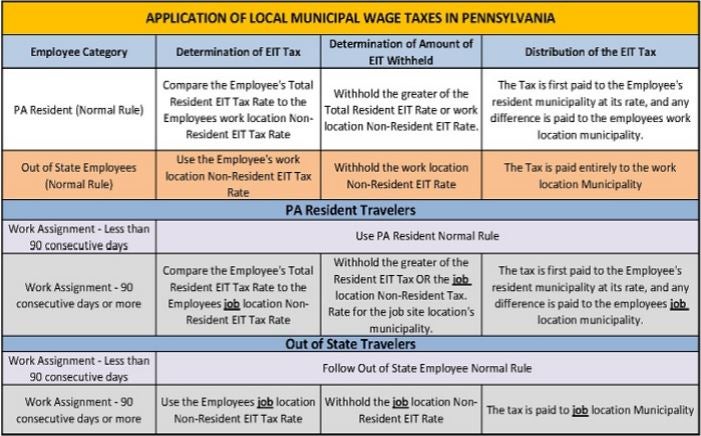

PA Resident Employees. Local earned income taxes for employees in Pennsylvania are political subdivision-based and divided with the local school district, depending on the employee’s residence. The EIT tax is assessed by the city, township, or borough (political subdivision) where the employee’s residence is located (for PA resident employees) and withheld and paid by the employer to the employee’s designated residence tax collector quarterly (“resident municipality”). For PA resident employees, in nearly all instances, the employee’s resident municipality will be paid its entire applicable EIT Tax, even when traveling and working at other job sites. The amount of EIT tax that is withheld is determined by comparing the employee’s residence EIT rate (“Total Resident EIT Rate”) to the municipality where the employee works (“Work Location Non-Resident EIT Rate”). Employers must always withhold the higher of the two, which would be 1.4% for the Example City.

-

PSD Codes. Political Subdivision Codes (“PSD Codes”) are a six digit code that identifies the employee’s residence municipality in question, as well as the employer’s work location municipality. These codes can be obtained from the PA.gov website, where employers can also obtain the applicable earned income tax rate, if any, for the political subdivision in question.

-

Out-of-State Employees. The Local Tax Enabling Act uses the term “non-resident” to refer to employees working in PA municipalities outside the employee’s PA resident municipality or domicile. This can be confusing and must be kept in mind when interpreting the tax for “out-of-state employees.”[5]

An employer must also complete the “Residency Certification Form” for all of its out-of-state employees. For an employee who lives out of state, the “Residence PSD Code” will be 88000 and the “Total Resident EIT Rate” will be 0%. EIT taxes for out-of-state employees must also be withheld based on where the employee works (“Work Location NonResident EIT Rate”), as well as the Local Services Tax (“LST”) based on the PA work location municipality. The employee must then apply for a credit if his or her local out-of state municipality also imposes a local earned income tax.

-

Travelers. Employers who have employees (PA residents or out-of-state employees) that travel to various job sites or assignments are required to withhold the EIT wage tax as follows:

-

Job Assignments of Less than Ninety Consecutive Days. If an employee works less than ninety consecutive days at a job location, employers must withhold the greater of the employee’s resident EIT tax (which is 0% for an out of state employee) or the employee’s Work Location Non-Resident EIT tax based on the location of the permanent home office of the employee. For the Example City, the amount withheld is 1.4%.

Accordingly, in this example, the employer’s office address will be deemed the employee’s permanent work location office, and the Example City will receive the entire 1.4% for an out-of-state employee. PA resident employees who travel to a job assignment that lasts less than ninety consecutive days will have their residence EIT tax paid to their resident municipality, and the difference, if any, (in this case

.4% for the Example City) will be paid their Employer’s work location municipality, with nothing being paid to the job location municipality.

-

Job Assignments of Ninety Consecutive Days or More. If the employee works ninety or more days at a job location, they are deemed to not have worked in their employer’s work location municipality for this period. The job site now is the “work location” for EIT tax purposes. Accordingly, for the period that they are traveling that equals or exceeds ninety consecutive days, employers must withhold the greater of the employee’s Resident EIT Tax (which is zero for an out-ofstate employee) or the employee’s Work Location Non-Resident Tax at the rate based on the job site location. Distribution of the withheld EIT tax will be as follows:

-

For a PA resident, employers would instruct its work location municipality’s tax collector to remit the resident’s EIT tax to its resident municipality, and any difference to the work location municipality, where the job is located. Usually there will be no difference, and the work location municipality will receive zero for the employee’s work. As set forth above, the PA resident’s resident municipality usually always gets its levied EIT tax.

-

For an out-of-state employee, employers would instruct its work location municipality’s tax collector to remit the entire EIT tax to the work location municipality where the job site is located. Nothing would be paid to their employer’s work location municipality in this case.

-

Example: If an employer sends a PA resident employee to a job site in Wheeling, West Virginia, and the employee reports directly to this job site for ninety or more consecutive days, the employer withholds no wage tax for the Example City for the employee. The employer would withhold and instruct its work location municipality’s tax collector to pay to the employee’s resident municipality the levied EIT tax for this PA resident.

-

Example: If an employer has a West Virginia employee who is sent to a job site in Uniontown, Pennsylvania, and the employee reports directly to this site for ninety or more consecutive days, the employer would withhold nothing for the Example City and would withhold and instruct its work location municipality’s tax collector to pay to Uniontown the entire applicable Work Location Non-Resident EIT tax for this employee.

-

Out-of-State Employees Who Report First to the Office Location and Travel to a Work Site for Ninety or More Consecutive Days.

The Example City may take the position that such employees are working out of the employer’s office at the Example City on a daily basis and not permanently assigned to any job site and demand that the entire 1.4% be paid.

In this situation, if the employee is assigned on a permanent basis to a job site located out of the Example City and works ninety or more consecutive days at that site, to avoid a dispute between the Example City and the job site municipality, you may want to eliminate the employee reporting daily to the employer’s office in the Example City for any purpose, such as to pick up a motor vehicle, and have the employee report directly to the job site for all purposes. Act 18 of 2018, does not offer much guidance on this issue, but it could be interpreted to require the payment of the EIT tax to the job site municipality and hence a dispute may develop.

The payment of taxes would be as outlined above for traveling employees. For PA residents as stated, the EIT tax would continue to be paid to their resident municipality, but if the job site EIT tax (Work Location Non-Resident EIT Tax) is greater, the difference would be paid to the job site’s municipal location. For an out-of-state employee, the entire EIT job site municipality’s tax would be paid to the job site’s municipal location at the Work Location Non-Resident EIT Rate.

-

Use of a Single Local Tax Collector. Employers with multiple work sites across the state of PA can remit their taxes to a single designated tax paying agency. This was created to simplify the tax payments and this process. This option is usually only utilized by extremely large employer with multiple work location sites and addresses. However, this will require the employer to remit the taxes monthly instead of quarterly. The assigned tax collector will disperse the same to the various municipalities.

-

Act 18 of 2018 and The Act 32 Policy and Procedural Manual. In May of 2018, Act 18 of 2018 amended the Local Tax Enabling Act and provided additional guidance. Also, on page 88 of The Act 32 Policy and Procedural Manual, the following was added this year with regard to traveling employees:

“Work Rules By Location”

How should employers withhold local EIT from employees who travel from site to site on a regular basis and do not maintain a place of employment in the areas where they work?

-

If an employee is working temporarily at a PA facility for a period of time that encompasses a “reporting quarter”, then the facility site would be the work location address used to determine the EIT rate and corresponding PSD code in the Address Search.

-

If an individual works for an employer who has a central business location in PA, but the employee “floats” or is transferred daily, weekly, or monthly between other business sites, then the central or main employer business location would be the work location address to determine the EIT rate and corresponding PSD code in the Address Search.

-

If an employee is hired by an employer and receives work orders or instructions at home in PA but physically reports to other business sites on a daily, weekly, or monthly basis, then the employee’s home address should be used as both the home and work location address used to determine the EIT rates and corresponding PSD codes in the Address Search.

Example 1 is the ninety consecutive day rule, but uses a “reporting quarter” for some unknown reason instead of ninety consecutive days. Employers would use the job’s work location address to determine the EIT rate for withholding purposes and compare this with the employee’s resident municipality rate to determine the higher of the two EIT tax withholding rates as set forth above.

Example 2 deals with the question of how to handle an employee who reports to the main office and picks up instruction and their vehicles, and then travels to a job site. In this situation, the example states that the employer’s central or main office is the work site for EIT purposes. Since the employee is a floater, he is not working at any one site for ninety or more consecutive days.

Example 3 is the situation where the employee physically reports to other businesses directly and receives his instructions at home. In this example, the employee’s resident home address is both the work and home location for EIT code purposes.

Below is an easy reference chart to assist employers in traversing through this EIT withholding maze.

[1] Act 18 of 2018 - Act of May 4, 2018, P.L. 102, No. 18

[2] P.L. 1257 No. 511 known as The Local Tax Enabling Act or Act 32.

[3] A “Nonresident” is defined in Act 18 of 2018 as: “A person or business domiciled outside the political subdivision levying the tax and performing services within the political subdivision levying the tax for at least 90 or more consecutive days.”

[4] It should be noted that the Employer’s work location municipality’s designated tax collecting entity, such as Keystone Collection Group for example, will do the actual disbursement of the taxes to the proper municipalities, however, the Employer is responsible for deducting the correct amount of tax and submitting the proper PSD codes for each of its employees to the tax collecting agency designated by the municipality.

[5] For purposes of this article, employees who reside in a state other than Pennsylvania will be referred to as “outof-state” employees and not as “non-residents.”