/>i

/>iIn a year characterized by the challenges of the COVID-19 pandemic and the potential for a change in U.S. presidential administration, SEC enforcement activity remained strong but PCAOB activity declined to a new low. Together, the SEC and PCAOB publicly disclosed 63 accounting and auditing enforcement actions during 2020, with nearly 80% representing SEC actions. Monetary settlements totaled more than $1.4 billion, nearly all of which was imposed by the SEC.

Research Sample and Data Sources

This research examines trends in accounting and auditing enforcement actions that were publicly disclosed by the U.S. Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB) between 2015 and 2020.

Accounting and auditing enforcement actions include (1) SEC Accounting and Auditing Enforcement Releases (AAERs) listed in the SEC Division of Enforcement Annual Reports and available on the SEC’s websit (“SEC actions”), and (2) PCAOB settled and adjudicated disciplinary orders available on the PCAOB’s website (“PCAOB actions”). SEC actions exclude follow-on administrative proceedings. SEC and PCAOB auditing actions exclude actions unrelated to the performance of an audit (e.g., failure to register with the PCAOB or to timely disclose certain reportable events to the PCAOB).

Respondents in PCAOB enforcement actions and SEC administrative proceedings and defendants in SEC civil proceedings are referred to as “respondents.” Respondents include (1) SEC registrants and audit firms (“firms”), and (2) individuals employed by or associated with SEC registrants and audit firms (“individuals” or “related individuals”).

Actions that involve one firm respondent are considered “non-U.S.” if the firm is headquartered outside the U.S. Actions that involve multiple firm respondents are considered “non-U.S.” if (1) all of the firm respondents are headquartered outside the U.S., or (2) one or more of the firm respondents are headquartered outside the U.S. and the alleged violations occurred outside the U.S. Actions that only involve individual respondents are considered “non-U.S.” if (1) the individuals are licensed or reside outside the U.S., and (2) the alleged violations occurred outside the U.S. All data are reported on a calendar year basis.

Actions involving restatements are actions that refer to an announcement that the company will restate, may restate, or has unreliable financial statements. Actions involving material weaknesses in internal control are actions that refer to an announcement that the company has a material weakness in internal control.

Monetary settlements include penalties, disgorgement, and prejudgment interest. Settlements include all actions settled during the year, regardless of when the action was initiated.

Accounting and Auditing Enforcement Activity in 2020

The SEC initiated 50 enforcement actions involving accounting and auditing allegations in 2020 against 36 individuals and 34 firms. Of the 50 enforcement actions, only four accounting and auditing actions were civil actions, with the remaining initiated as administrative proceedings. In 2020, 71 respondents settled charges that the SEC had brought in 2020 and in prior years. Monetary settlements were imposed on 53 (75%) of those respondents and totaled approximately $1.4 billion. In 23 of the 71 settlements, the SEC reported that it took into account the respondent’s self-reporting, cooperation, and/or remedial efforts as it set penalties and other remedies.

The PCAOB publicly disclosed 13 enforcement actions involving auditing in 2020, just over half of the 24 actions disclosed in 2019.[1] Of the 27 individual and firm respondents that settled with the PCAOB in 2020, monetary settlements were imposed on 19 (70%). Monetary settlements totaled almost $1.5 million.

SEC Actions Involving Accounting and Auditing Declined in 2020

-

The total number of accounting and auditing actions initiated by the SEC in 2020 declined 14% from 58 to 50. This was a 17% decrease from the average number of 60 initiated actions in the 2015–2019 period.

-

During 2020, the SEC brought 46 (92%) administrative proceedings, with all but one announcing a concurrent settlement on the same day.

-

The SEC also brought four (8%) civil actions. All but one of these civil actions were resolved by the end of 2020.

SEC Actions Involving Accounting and Auditing by Year Initiated

2015–2020

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

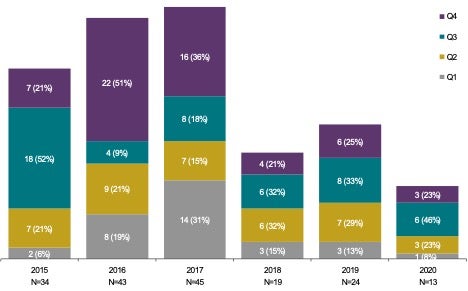

The Decrease in SEC Actions Resulted from a Substantial Decline in the First Quarter

-

The SEC initiated only three accounting and auditing enforcement actions in Q1 2020, the lowest level of activity for any quarter from 2015 through 2020 and less than 20% of the average Q1 enforcement level over the last five years.

-

Actions initiated in Q2 through Q4 of 2020 returned to the levels experienced in 2019.

-

More than half of the actions in 2020 were initiated in Q3 (27), compared to one-third on average in Q3 of 2015–2019.

Quarterly SEC Actions Involving Accounting and Auditing by Year Initiated

2015–2020

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

After the First Quarter, SEC Activity Recovered to 2019 Levels

-

Relative to Q1 2019, which was affected by the government shutdown for most of January, SEC enforcement activity in Q1 2020 was particularly slow. The SEC did not initiate any actions in March 2020.

-

However, SEC enforcement activity recovered in Q2 2020 as staff from the Division of Enforcement transitioned to a remote working environment.[2]

-

During the last week of Q3 2020, which marks the end of the SEC fiscal year, the SEC initiated 13 actions. A similar uptick in initiated actions also occurred at the end of Q3 2019.

SEC Actions Involving Accounting and Auditing, by Date Initiated

2019–2020

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

The Percentage of Non-U.S. Actions Brought by the SEC Was Consistent with Prior Years

-

The percentage of non-U.S. actions brought by the SEC was lower in 2020 (14%) compared to 2019 (17%) but in line with the 2015–2019 average (14%).

-

Of the seven non-U.S. actions, five (71%) actions involved internal control over financial reporting and one action involved auditing allegations.

-

Since 2015, the SEC has brought actions involving respondents in 24 countries outside the U.S. The most actions (four each) have been brought against respondents in Brazil, Canada, India, Japan, Mexico, and the United Kingdom.

SEC Actions Involving U.S. and Non-U.S. Respondents by Year Initiated

2015–2020

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

The Percentage of SEC Actions Involving Announced Restatements and/or Material Weaknesses in Internal Control Was Consistent with 2019

-

Of the 50 SEC enforcement actions in 2020, 18 involved announced restatements and 11 involved announcements of material weaknesses in internal control.

-

The percentage of 2020 SEC actions involving announced restatements and/or material weaknesses in internal control (40%) was higher than the 2015–2019 average (36%).

-

Of the 18 actions involving restatements in 2020, 15 alleged improper revenue recognition.

SEC Actions Involving Announcements of Restatements and/or Internal Control Weaknesses

by Year Initiated

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

Internal Control Over Financial Reporting and Revenue Recognition Were the Most Common Allegations in 2020 SEC Actions

-

Of the 50 actions brought by the SEC in 2020, about one-third alleged revenue recognition violations and more than half alleged violations related to a company’s internal control over financial reporting.

-

Of the 12% of the actions brought by the SEC that related to auditing, the majority involved allegations concerning audit documentation and/or supervision of the audit.

SEC Actions Involved Fewer Respondents in 2020

-

There were 70 total respondents in the actions initiated by the SEC in 2020, 29% below the 2015–2019 average.

-

The number of individual respondents remained at the level in 2019, 43% below the average number of 63 respondents in the prior four years.

-

In 2020, 49% of the respondents were firms, up from the 2015–2019 average of 43%.

Respondents in SEC Accounting and Auditing Actions by Year Initiated

2015–2020

|

2015–2019 |

2019 |

2020 |

||||

|

Average |

Share |

Number |

Share |

Number |

Share |

|

|

Number of Actions |

||||||

|

Individual(s) |

21 |

35% |

20 |

34% |

18 |

36% |

|

Firm(s) |

23 |

39% |

29 |

50% |

25 |

50% |

|

Firm(s) and Individual(s) |

16 |

26% |

9 |

16% |

7 |

14% |

|

Total |

60 |

100% |

58 |

100% |

50 |

100% |

|

Number of Respondents |

||||||

|

Individuals |

57 |

57% |

36 |

47% |

36 |

51% |

|

Firms |

42 |

43% |

40 |

53% |

34 |

49% |

|

Total |

99 |

100% |

76 |

100% |

70 |

100% |

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: New SEC enforcement actions are those that were initiated in each year. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

The Majority of SEC Actions Involved SEC Registrants and Related Individuals

-

The number of SEC actions involving SEC registrants and related individuals increased by 35% in 2020 to 58 from 43 actions in 2019.

-

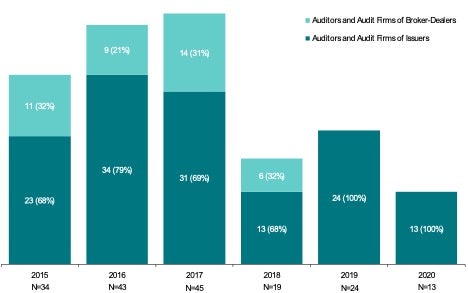

SEC actions involving auditors and audit firms declined by 64% in 2020 to 12 from 33 actions in 2019.

-

There were no actions involving auditors or audit firms of broker-dealers in 2020.

Respondents in SEC Actions by Year Initiated

2015–2020

Source: SEC Annual Enforcement Reports and Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

Total Monetary Settlements in 2020 SEC Actions Were Approximately $1.4 Billion

-

In addition to bars, suspensions, and other nonmonetary sanctions, the SEC imposed monetary settlements against 75% of the respondents for a total of approximately $1.4 billion.

-

Total monetary settlements against firms comprised the vast majority of the $1.4 billion settlement total. Total monetary settlements against firms increased in 2020, but the median settlement decreased from $4.1 million in 2019 to $3.4 million in 2020. Two firms paid total monetary settlements of at least $100 million each in 2020.

-

Total monetary settlements against individuals were approximately $3.9 million, $44.8 million lower than in 2019. The median settlement increased from $50,000 in 2019 to $75,000 in 2020.

Monetary Settlements in Resolved SEC Actions

2018–2020 ($ amounts in thousands)

|

|

2018 |

2019 |

2020 |

|||

|

|

Individuals |

Firms |

Individuals |

Firms |

Individuals |

Firms |

|

Total Respondents |

43 |

56 |

33 |

37 |

36 |

35 |

|

Respondents Fined |

29 |

43 |

25 |

31 |

25 |

28 |

|

Average Settlement |

$104 |

$49,884 |

$1,948 |

$20,040 |

$156 |

$50,104 |

|

Median Settlement |

$25 |

$1,500 |

$50 |

$4,125 |

$75 |

$3,350 |

|

Max Settlement |

$1,656 |

$1,786,674 |

$43,700 |

$147,000 |

$550 |

$1,006,300 |

|

Total Settlements |

$3,013 |

$2,145,017 |

$48,695 |

$621,236 |

$3,910 |

$1,402,923 |

Source: Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: The totals above include monetary penalties of $5,028 in 2019 for an individual that were waived based upon the respondent’s sworn representations about his financial condition and $606.3 million in 2020 for disgorgement that was deemed satisfied by a payment paid to a third party. The amounts above for “firms” include $40.1 million in 2019 for monetary settlements to be paid “jointly and severally” between a firm and individual. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

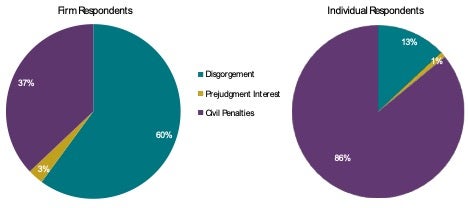

Disgorgement and Prejudgment Interest Comprised 63% of Total SEC Settlements

-

For firm respondents, disgorgement and civil penalties accounted for approximately 60% and 37% of all monetary settlements, respectively, while prejudgment interest accounted for the remaining 3%.

-

Some of the largest disgorgement amounts were imposed after the U.S. Supreme Court decision in Liu v. SEC on June 22, 2020.[3] In particular, 97% of the total disgorgement amount charged by the SEC in 2020 was imposed after the Liu decision.

-

For individual respondents, disgorgement and civil penalties accounted for approximately 13% and 86% of all monetary settlements, respectively, while prejudgment interest accounted for the remaining 1%.

-

In 23 settlements, the SEC reported that it took into account the respondent’s self-reporting, cooperation, and/or remedial efforts as it set penalties and other remedies. These mitigating factors were applied to 19 firm respondents and four individual respondents.[4]

Monetary Settlements in SEC Actions by Respondent Type

2020

Source: Accounting and Auditing Enforcement Releases (AAERs), available at https://www.sec.gov.

Note: The totals above include $606.3 million for disgorgement that was deemed satisfied by a payment paid to a third party. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

PCAOB Enforcement Activity Decreased to a Level Well Below Recent Years

-

As required by the Sarbanes-Oxley Act, the PCAOB keeps its investigations and disciplinary proceedings confidential and nonpublic until the matter is settled or otherwise finalized.[5]

-

PCAOB enforcement actions decreased 46% in 2020 compared to 2019.

-

At 13, the number of PCAOB actions in 2020 was 39% of the 2015–2019 average and was the lowest number of actions disclosed in the last six years.

-

In 2020, for the second year in a row, the PCAOB did not disclose any actions pertaining to audits of broker-dealers. In the prior four years, actions involving auditors and audit firms of broker-dealers comprised nearly 30% of all actions on average.

PCAOB Actions Involving Auditing by Year Finalized

2015–2020

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

PCAOB Actions Decreased Each Quarter of 2020 Compared to Each Respective Quarter in 2019

-

Unlike SEC actions, finalized PCAOB actions did not return to pre-pandemic levels after Q1 2020.

-

For each quarter in 2020, the number of finalized PCAOB actions was equal to or lower than that for each respective quarter over at least the last three years.

-

Nearly 70% of 2020 PCAOB actions involved alleged violations of the Engagement Quality Review (EQR) standard, up from a third of the actions in 2019.

-

Two-thirds of the 2020 actions involving firm respondents contained allegations related to the firm’s system of quality control, down from 77% in 2019.

Quarterly PCAOB Actions Involving Auditing by Year Finalized

2015–2020

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

Fewer PCAOB Actions Involved Non-U.S. Respondents

-

The percentage of PCAOB actions involving non-U.S. respondents in 2020 (8%) decreased substantially compared to 2019 (29%) and the 2015–2019 average (25%).

-

The one non-U.S. action involved an audit firm and two auditors in Australia. Since 2015, the PCAOB has brought actions involving respondents in 15 countries outside the U.S. The most actions have been brought against auditors and audit firms in Brazil.

PCAOB Actions Involving U.S. and Non-U.S. Respondents by Year Finalized

2015–2020

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

Nearly 40% of PCAOB Actions Involved Announced Restatements and/or Material Weaknesses in Internal Control

-

The proportion of PCAOB actions in 2020 involving announced restatements and/or material weaknesses in internal control (38%) was more than double the 2015–2019 average (15%).

-

Unlike 2019, when the majority of PCAOB actions with an announced restatement and/or material weakness in internal control involved revenue recognition, only one action in 2020 involved revenue recognition.

PCAOB Actions Involving Announcements of Restatements and/or Internal Control Weaknesses by Year Finalized

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

The Number of Unique PCAOB Actions Substantially Decreased

-

At times, PCAOB actions involve other relevant entities and/or individuals. The PCAOB identifies related actions that are settled or otherwise finalized as a separate action. In certain instances, related actions were settled on different dates and/or included different allegations.

-

Of the 13 PCAOB actions in 2020, three (23%) were identified by the PCAOB as being related to other action(s), consistent with prior years.

-

In 2020, there were 10 unique PCAOB actions, a 60% decrease from the 2015–2019 average (25), and a 71% decrease from the peak in 2017 (35).

Unique PCAOB Actions by Year Finalized

2015–2020

|

2015–2019 |

2019 |

2020 |

||||

|

Average |

Share |

Number |

Share |

Number |

Share |

|

|

Related Actions |

8 |

24% |

6 |

25% |

3 |

23% |

|

Unique Actions |

25 |

76% |

18 |

75% |

10 |

77% |

|

Total Actions |

33 |

100% |

24 |

100% |

13 |

100% |

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: PCAOB enforcement actions are actions that were publicly disclosed in each year. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis

PCAOB Actions Involved Substantially Fewer Respondents in 2020

-

The total number of respondents in 2020 PCAOB actions decreased 33% from 2019 and was about half of the 2015–2019 average.

-

In 2020, almost two-thirds of the actions involved a firm and at least one individual auditor, up from the 2015–2019 average of 46%.

Respondents in PCAOB Actions by Year Finalized

2015–2020

|

2015–2019 |

2019 |

2020 |

||||

|

Average |

Share |

Number |

Share |

Number |

Share |

|

|

Number of Actions |

||||||

|

Individual(s) |

11 |

33% |

11 |

46% |

4 |

31% |

|

Firm(s) |

7 |

21% |

4 |

16% |

1 |

8% |

|

Firm(s) and Individual(s) |

15 |

46% |

9 |

38% |

8 |

61% |

|

Total |

33 |

100% |

24 |

100% |

13 |

100% |

|

Number of Respondents |

||||||

|

Individuals |

30 |

57% |

27 |

68% |

18 |

67% |

|

Firms |

23 |

43% |

13 |

32% |

9 |

33% |

|

Total |

53 |

100% |

40 |

100% |

27 |

100% |

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: PCAOB enforcement actions are actions that were publicly disclosed in each year. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

Total Monetary Settlements in 2020 PCAOB Actions Were Approximately $1.5 Million

-

In addition to bars, suspensions, and other nonmonetary sanctions, the PCAOB imposed monetary settlements against 70% of respondents in 2020, up from 60% in 2019. The increase was driven by the imposition of monetary settlements against 67% of individuals, up from 48% in 2019.

-

The PCAOB imposed monetary settlements against 78% of firms in 2020, down from 85% in 2019.

-

Total monetary settlements against individuals were $180,000, which was $15,000 higher than in 2019. The median settlement increased from $10,000 in 2019 to $15,000 in 2020.

-

Total monetary settlements against firms were $1,290,000 in 2020, $490,000 lower than in 2019. The median settlement in 2020 remained unchanged from 2019, but the average settlement in 2020 against firms increased 14% from the 2019 average.

Monetary Settlements in Settled PCAOB Actions

2018–2020 ($ amounts in thousands)

|

|

2018 |

2019 |

2020 |

|||

|

|

Individuals |

Firms |

Individuals |

Firms |

Individuals |

Firms |

|

Total Respondents |

18 |

13 |

27 |

13 |

18 |

9 |

|

Respondents Fined |

7 |

11 |

13 |

11 |

12 |

7 |

|

Average Settlement |

$26 |

$94 |

$13 |

$162 |

$15 |

$184 |

|

Median Settlement |

$25 |

$15 |

$10 |

$50 |

$15 |

$50 |

|

Max Settlement |

$50 |

$500 |

$25 |

$500 |

$25 |

$750 |

|

Total Settlement |

$180 |

$1,035 |

$165 |

$1,780 |

$180 |

$1,290 |

Source: Settled Disciplinary Orders, Adjudicated Final Board Disciplinary Actions, available at https://pcaobus.org.

Note: PCAOB enforcement actions are actions that were publicly disclosed in each year. See Research Sample and Data Sources for additional information, available at https://www.cornerstone.com/Publications/Reports/Accounting-Auditing-Enforcement-Activity-2020-Review-Analysis.

The views expressed herein are solely those of the authors, who are responsible for the content, and do not necessarily reflect the views of Cornerstone Research.

[1] As required by the Sarbanes-Oxley Act, the PCAOB keeps its investigations and disciplinary proceedings confidential and nonpublic until the matter is settled or otherwise finalized. See “Enforcement,” PCAOB website, https://pcaobus.org/Enforcement/Pages/default.aspx.

[2] In a speech on October 8, 2020, then SEC Chair Jay Clayton stated, “I am pleased to report that while the pandemic significantly impacted how we do our work, it did not negatively impact the work itself.” Jay Clayton, “An Update on FY 2020 Results,” Remarks at SEC Speaks, Washington D.C., October 8, 2020, https://www.sec.gov/news/speech/clayton-sec-speaks-2020-10-08. See also Stephanie Avakian, “Protecting Everyday Investors and Preserving Market Integrity: The SEC’s Division of Enforcement,” Remarks at the Institute for Law and Economics, University of Pennsylvania, September 17, 2020, https://www.sec.gov/news/speech/avakian-protecting-everyday-investors-091720 (“Since mid-March, the entire Division [of Enforcement] has been working from home. . . . [S]ince mid-March, the Commission has filed more than 325 new enforcement actions.”).

[3] In Liu v. SEC, the Supreme Court held that disgorgement awards sought by the SEC in federal courts are an equitable remedy permitted by the federal securities laws if capped to the wrongdoer’s net profits and awarded for the benefit of wronged investors. See Stephanie Avakian, “Protecting Everyday Investors and Preserving Market Integrity: The SEC’s Division of Enforcement,” Remarks at the Institute for Law and Economics, University of Pennsylvania, September 17, 2020, https://www.sec.gov/news/speech/avakian-protecting-everyday-investors-091720. See also Liu et al. v. Securities and Exchange Commission, No. 18-1501, 591 U.S. ___ (2020), https://www.supremecourt.gov/opinions/19pdf/18-1501_8n5a.pdf.

[4] In a speech on September 17, 2020, then SEC Division of Enforcement Director Stephanie Avakian stated, “We have also focused on rewarding and messaging the benefits of cooperation. We recognize the value in providing greater transparency into how the Commission considers and weighs cooperation credit – meaningful cooperation can substantially accelerate an investigation, which is in everyone’s interest. We have tried to message more clearly the benefits of cooperation and in a number of instances the Commission has provided that information in its orders.” Stephanie Avakian, “Protecting Everyday Investors and Preserving Market Integrity: The SEC’s Division of Enforcement,” Remarks at the Institute for Law and Economics, University of Pennsylvania, September 17, 2020, https://www.sec.gov/news/speech/avakian-protecting-everyday-investors-091720.

[5] See “Enforcement,” PCAOB website, https://pcaobus.org/Enforcement/Pages/default.aspx.